The Quiet Reshuffle of the Private Rented Sector

image from property 118

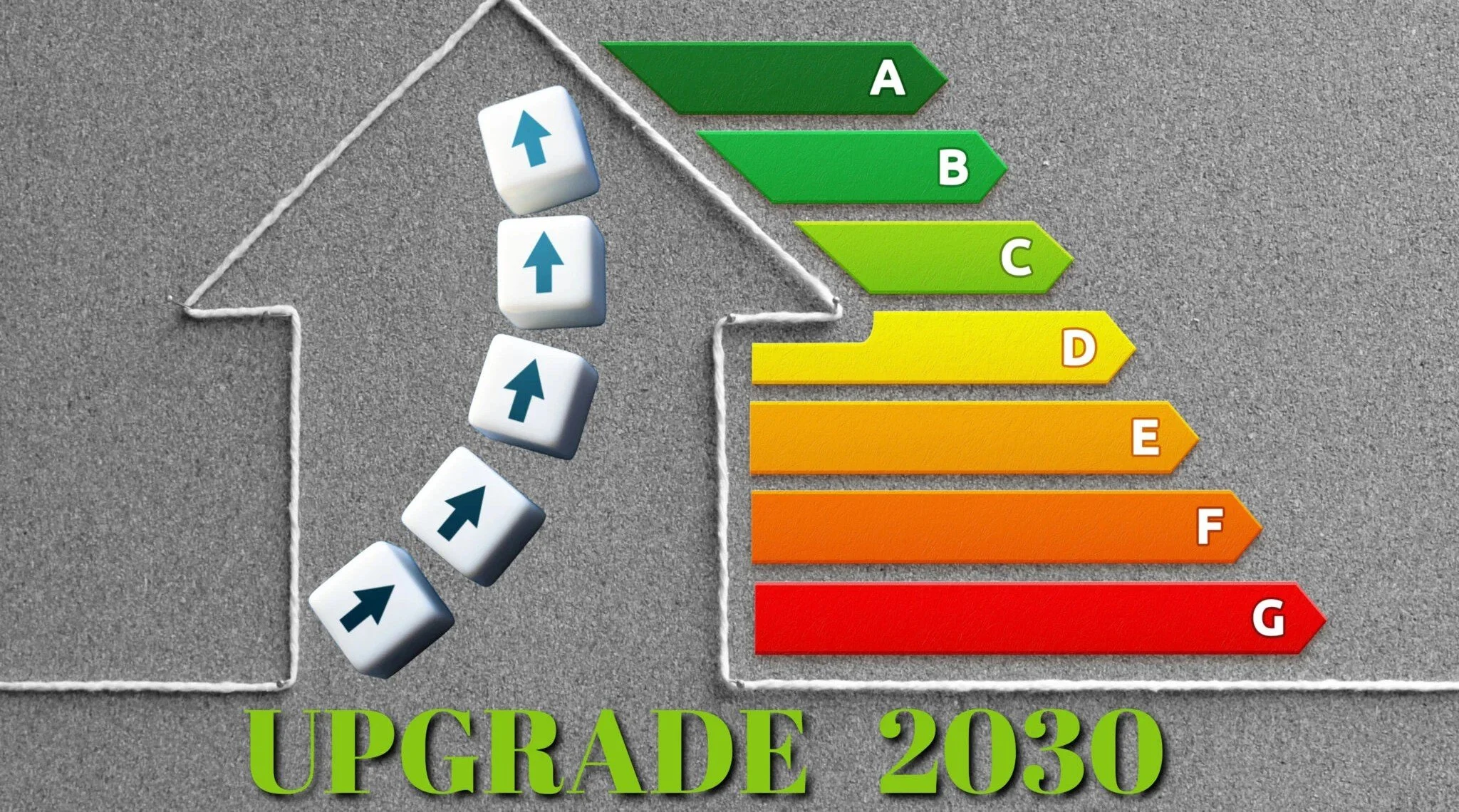

Why the new EPC and Decent Homes trajectory matters far more than people realise

If you take the government’s updated Decent Homes Standard and revised MEES direction at face value, and then run it forward using reasonable assumptions, you don’t get a gentle adjustment to the private rented sector.

You get a violent reshuffling.

Not an overnight collapse.

Not an apocalypse.

But a multi-year sorting mechanism that strands some stock, squeezes certain landlords out, reprices whole sub-markets, and quietly advantages those who create new, rental-grade dwellings over those trying to preserve legacy stock.

What follows is a sector-level model: Who gets squeezed, what becomes non-viable, how behaviour shifts, and why tenants ultimately sit downstream of all of it.

1. Why “four years” is genuinely short in housing

October 2030 sounds comfortably distant if you’re thinking politically.

It’s not distant at all in housing terms.

EPC and MEES compliance is not a cosmetic exercise. It involves:

material capex

design decisions

installer availability

tenant access and disruption

void planning

financing and re-valuation risk

Add to that a simple behavioural reality: Many landlords will not act until rules are final and enforcement feels real.

Now layer in the structure of the sector itself. A large proportion of the PRS is held by:

small landlords

one to three properties

limited balance sheets

limited appetite for repeated regulatory projects

So while the deadline is 2030, the market reaction starts much earlier.

A realistic mental model looks something like this:

2026–2027: denial / wait-and-see

2027–2028: cost discovery and early exits

2028–2029: scramble, installer bottlenecks, rising costs

2029–2030: forced decisions and accelerated disposals

By the time enforcement arrives, much of the repricing has already happened.

2. The key concept: “stranded stock”

The most important shift isn’t that the bar is being raised.

It’s that the bar itself is being rebuilt.

A fabric-first, energy-system-aware approach doesn’t just ask how efficient a home is — it asks whether it can realistically be upgraded to operate in a decarbonising system.

That creates a class of housing that is simply “hard to treat”, particularly:

solid wall terraces

flats in blocks where landlords don’t control the envelope

conservation areas with planning constraints

electrically constrained properties

awkward layouts where heat distribution and ventilation upgrades are invasive

The result is a new category in the market:

Homes that are perfectly fine to live in.

Perfectly fine to sell to an owner-occupier.

But increasingly non-viable to rent.

Historically, owner-occupier viability and rental viability overlapped heavily.

This policy pulls them apart.

That’s a structural change.

3. How landlords are likely to behave (natural assumptions)

Assume the following, none of which are extreme:

A meaningful share of PRS stock requires more than light-touch upgrades

Installer capacity tightens as deadlines approach

Costs rise non-linearly

Many landlords are already fatigued by tax, regulation, and interest rates

From there, behaviour becomes fairly predictable.

A) Early exit by small landlords

Landlords with:

low yields

older stock

limited cash reserves

are unlikely to embark on multi-stage retrofit programmes.

They sell.

Often into the owner-occupier market.

That increases sales supply — but permanently reduces rental supply, because many of those homes don’t come back into the PRS.

B) Consolidation by “capex-capable” operators

Larger or more professional landlords — those with:

project management capability

access to finance

portfolio-level planning

will buy discounted stock and upgrade it.

The outcome isn’t fewer homes.

It’s fewer landlords, holding more homes.

C) Rent pressure intensifies, even if prices soften

This is the part policymakers often underestimate.

If rental supply falls faster than demand, rents rise.

And when compliance raises operating costs, landlords who remain in the sector price that risk in.

So you can quite plausibly see:

house prices stagnating or softening in some segments

rents rising at the same time

That combination is politically awkward — but economically coherent.

4. Near-term mechanics: repricing, not a cliff edge

This isn’t a sudden ban. It’s a sorting process with a deadline.

Expect widening spreads between:

Turnkey, compliant rentals (premium pricing, high liquidity)

“Needs upgrade” stock (discounted for capex, hassle, and risk)

Hard-to-treat / exemption-reliant stock (discounted further, regulatory overhang)

Owner-occupier-only stock (priced on different fundamentals entirely)

The closer we move toward 2030, the sharper those spreads become.

That’s not collapse.

It’s stratification.

5. What tenants experience (second-order effects)

Tenants don’t experience policy through consultation documents.

They experience it through availability, price, and choice.

If we assume a net reduction in PRS supply in certain areas, tenants feel it as:

fewer listings

higher rents

tighter affordability checks

more competition

increased churn when properties are sold or taken out for upgrade

Exemptions don’t create homes.

They just delay compliance.

So the policy improves quality for some tenants …while increasing access pressure for others.

That trade-off is rarely stated explicitly.

6. Why creators of new dwellings are structurally advantaged

This is the crucial asymmetry.

If you are creating dwellings, conversions, redevelopment, net-add supply, you can:

design to the new metrics from day one

integrate fabric, heating, and energy systems properly

avoid retrofit complexity

bake compliance into funding, valuation, and exit assumptions

That is a genuine strategic advantage.

And it’s also the missing half of the policy conversation.

Standards without supply don’t raise outcomes.

They ration access.

7. Likely winners and losers by 2030

A simplified sector map looks like this:

Group Small thin-margin landlords

Likely outcome Partial exit / sell-down

Group Large professional operators

Likely outcome Consolidate + upgrade + higher rents

Group Hard-to-treat legacy stock

Likely outcome Discounted + exempted + churn

Group Turnkey compliant rentals

Likely outcome Premium pricing + strong liquidity

Group Net-new dwelling creators

Likely outcome Structural tailwind + revaluation uplift

Group Lower-income tenants

Likely outcome Higher competition + affordability pressure

This isn’t ideological.

It’s mechanical.

8. The emergence of a “rental-grade” asset class

Quietly, this policy creates a new definition of quality:

Rental-grade housing

Homes that are compliant, efficient, electrification-ready, and future-proofed.

That matters because rental-grade assets are:

easier to finance

easier to insure

easier to value

and more institutionally attractive

Over time, expect:

lenders to price future compliance risk explicitly

valuers to apply “compliance haircuts” to legacy stock

portfolios to be assessed on upgrade readiness, not just yield

This is entrepreneurial housing infrastructure in practical terms.

Not ideology.

Not virtue signalling.

Just housing designed to function as modern infrastructure, rather than patched-up legacy shelter.

Final thought

If regulation makes legacy stock harder to operate, capital must move toward creating new supply.

If it doesn’t, tenants lose.

That’s the real tension in this debate, and it’s the part we should probably be talking about far more openly.

For a deeper exploration of these ideas

including frameworks like The Unicorn Model and Creator OS, get your copy of Property Unicorns and join the movement redefining what it means to build Britain’s future.