From Fighter Jets to Property Unicorns: Rob Stewart on Mixed-Use Property, Housing Supply and Smarter Investing

Rob Stewart’s route into property was not polished, easy or guru-led. It was built through mistakes, market cycles, hard lessons and a shift from chasing yield to creating real value through mixed-use buildings, regeneration and housing supply.

Most property content online is built around one fantasy: fast money, low effort, instant freedom.

Rob Stewart’s approach is the opposite.

In this YouTube podcast, hosted by Allsorts Property with Joe Burns, Rob talks about the reality of building wealth through property investing: the mistakes, the market shifts, the painful lessons, and why he now believes the future belongs to investors who create housing supply, understand mixed-use property, and stop chasing flimsy paper yield.

This is not guru property talk. It is grounded, commercial and brutally practical.

Why Rob Stewart’s property strategy changed

Rob did not enter property through a polished blueprint. After leaving the RAF, where he flew fighter jets and trained pilots, he moved into property during a very different market cycle. In those early years, like many investors, he started with the classic buy-refurbish-refinance approach and lower-value single lets.

It worked for a time.

But over the years, the bigger lesson became clear: high-yield property is not always high-profit property.

That is where Rob’s thinking shifted. Instead of chasing properties that looked good on paper, he started focusing on assets that gave him stronger control over cash flow, value creation and long-term resilience. That led him deeper into HMOs, mixed-use buildings, commercial units, flats above shops, and commercial-to-residential opportunities.

The result is what he now calls the Property Unicorn model.

What is a property unicorn?

A property unicorn, in Rob’s world, is not just a quirky mixed-use building.

It is a property deal that can create serious value quickly, without relying on drawn-out planning battles or high-risk heavy development. The focus is on adding value through strategy, structure, income optimisation, lease engineering, density and smarter use of space.

That matters because many investors are still using outdated models in a market that has changed.

Rob’s argument is simple: the old low-margin buy-to-let approach is not dead in every case, but for many investors it is no longer the best route to significant income or scalable growth. Mixed-use property, commercial conversions and multi-income assets often offer better upside, better negotiation opportunities, and more ways to force appreciation.

The real opportunity in mixed-use property

One of the most interesting parts of the conversation is Rob’s case for mixed-use property investing.

This is the territory many residential investors avoid because commercial space feels unfamiliar. But that is exactly where some of the opportunity sits. Fewer buyers understand the model. Fewer buyers are comfortable underwriting it. That often creates better buying conditions for investors who know what they are doing.

Rob explains why he prefers buildings with multiple income streams and why he sees value in assets that combine retail units, self-contained flats, and operational flexibility.

This is also where the conversation gets bigger than just investment returns.

Because for Rob, mixed-use property is not just about making money. It is about bringing underused buildings back into use, increasing housing density, regenerating urban areas, and creating assets that serve how people actually want to live now.

That is a much more relevant conversation than another shallow debate about whether buy-to-let is dead.

Rob Stewart on the UK housing crisis and rental market

Another strong thread running through the episode is Rob’s view on the UK housing crisis, rental supply, and the relationship between private landlords and the public sector.

His position is refreshingly unsentimental.

He is not pretending landlords are charities. Property investing is a profit business. But he is also clear that the UK needs more housing, more intelligent regeneration, and better ways to bring private capital into solving real supply problems.

That is where Rob’s thinking stands out.

Instead of defaulting to left-versus-right political noise, he argues for practical alignment: if the public sector wants more homes created, more empty buildings brought back into use, and better accommodation for people who need it, then private investors and developers have to be incentivised properly to deliver that.

That point alone makes the podcast worth watching.

Because whether you agree with him or not, Rob is talking about the future of housing, regeneration, rental supply and property development in a far more serious way than most of the online property world.

The biggest mistake property investors make

The episode also lands on a point that applies well beyond this one conversation.

Most property investors think the game is about finding deals.

Rob argues it is really about understanding vendor motivation, negotiation, process and market knowledge.

That means knowing your area properly. Knowing what streets work and what streets do not. Knowing price per square foot. Knowing rents. Knowing where value can be unlocked. And then building a boring, repeatable acquisition machine instead of waiting for magic to appear on Rightmove.

That is a much more mature view of property sourcing and deal analysis, and it is one of the reasons Rob’s content cuts through.

Why this YouTube episode is worth your time

This is not a podcast built on empty inspiration.

It is a conversation about how serious investors adapt when markets change. It covers property strategy, mixed-use investing, HMOs, commercial property, housing supply, negotiation, regeneration, landlord economics and performance.

It also gives you a much clearer sense of who Rob Stewart is and how he thinks.

If you are interested in UK property investing, especially beyond basic buy-to-let, this is exactly the kind of conversation worth paying attention to.

Watch the full episode below.

Incentives Don’t Wait for Legislation: What the Section 21 Evictions Story Actually Reveals

Recent coverage in The Negotiator highlighted accusations that a Labour donor’s property company has issued large numbers of eviction notices ahead of the proposed abolition of Section 21.

The story has triggered predictable reactions.

Criticism of landlords.

Political concern.

Debate around whether such actions align with the “spirit” of the legislation.

On the surface, it appears to be another flashpoint in the ongoing tension between tenant protection and landlord behaviour.

But step back, and the situation looks very different.

Because what is being reported is not an isolated incident.

It is a predictable response to a policy signal

Recent coverage in The Negotiator highlighted accusations that a Labour donor’s property company has issued large numbers of eviction notices ahead of the proposed abolition of Section 21.

The story has triggered predictable reactions.

Criticism of landlords.

Political concern.

Debate around whether such actions align with the “spirit” of the legislation.

On the surface, it appears to be another flashpoint in the ongoing tension between tenant protection and landlord behaviour.

But step back, and the situation looks very different.

Because what is being reported is not an isolated incident.

It is a predictable response to a policy signal.

From a policy perspective, the proposed removal of Section 21 represents a significant shift in how control over residential property is exercised. Landlords are being told, in effect, that their ability to regain possession of an asset will become more restricted and more conditional.

Once that signal is clear, behaviour begins to adjust.

Not after implementation.

Before it.

For larger operators, this adjustment can take the form of coordinated action across portfolios. For smaller landlords, it may result in earlier sales, reduced investment, or a gradual withdrawal from the market.

In both cases, the underlying driver is the same.

Incentives change, and behaviour follows.

What has made this particular case more visible is the scale of the operator involved and its political associations.

A “Labour donor landlord” issuing eviction notices ahead of a Labour-led policy change is, understandably, a compelling headline.

But focusing too heavily on the identity of the actor risks obscuring the more important point.

The behaviour itself is entirely consistent with the incentives created by the policy.

This becomes clearer when we examine how similar actions are interpreted across different parts of the market.

When individual landlords issue eviction notices in response to regulatory pressure, the language used is often moral. They are described as opportunistic or exploitative, contributing to a narrative that places responsibility at the level of the individual.

When institutional or large-scale operators take the same action, the framing shifts. The language becomes operational. Decisions are described as portfolio management, risk mitigation, or standard business practice.

The action is the same.

The interpretation is not.

This distinction matters because it reflects a deeper structural shift within the UK housing market.

Housing policy does not affect all participants equally. It interacts with scale.

Large operators have the ability to model policy risk, act early, and absorb transitional disruption. They can respond to legislative signals with speed and coordination, often positioning themselves ahead of the market.

Smaller landlords operate under different constraints. Their exposure is concentrated. Their margins are tighter. Their ability to absorb prolonged uncertainty is limited.

As regulatory pressure increases, the impact is cumulative.

It is rarely a single policy that forces change, but the gradual layering of complexity, compliance, and risk.

The proposed abolition of Section 21 is often framed as a necessary step towards improving tenant security, and in many respects, that objective is valid.

However, focusing solely on the intended outcome risks overlooking the behavioural consequences.

Because policy does not just set rules.

It reshapes incentives.

And when incentives are altered without fully accounting for how different actors respond, the outcomes can diverge significantly from the intention.

In this case, signalling a reduction in landlord control creates a clear incentive to act before that control is removed.

For a large operator, that may involve issuing eviction notices across a portfolio in advance of legislative change.

For a smaller landlord, it may mean exiting the market entirely or choosing not to re-enter.

The forms differ.

The direction is the same.

This is where the discussion moves beyond the specifics of one company or one set of eviction notices.

The more important question is what kind of housing market these dynamics produce over time.

If policy consistently increases regulatory friction, uncertainty, and operational complexity, participation becomes more selective.

Those with the capacity to absorb and manage that friction remain.

Those without it gradually step away.

The result is not immediate, but it is directional.

Markets begin to consolidate.

Scale becomes an advantage not just in efficiency, but in resilience.

And over time, control shifts.

The current reaction to “mass evictions ahead of the Section 21 ban” reflects a desire to interpret events through a moral lens.

To identify bad actors.

To assign responsibility.

To respond to the optics.

But housing markets do not operate on optics.

They operate on incentives.

If the incentives created by policy encourage early action, early action will occur.

If they increase risk for smaller participants, those participants will reduce their exposure or exit.

If they favour those who can model and absorb uncertainty, those actors will gradually dominate.

None of this requires coordination or intent.

It is an emergent outcome of system design.

Which brings us to the more difficult, and more important, question.

Is the current direction of UK housing policy designed to improve outcomes within the existing structure…

or is it, intentionally or not, reshaping who that structure ultimately serves?

Because if the long-term effect of regulatory change is to concentrate ownership and control within fewer, larger entities, then the conversation around tenant protection cannot be separated from the question of market composition.

The events highlighted in recent reporting are not an anomaly.

They are an early signal.

And if the underlying incentives remain unchanged, they are unlikely to be the last.

Rob Stewart

For much of the past decade, Britain’s housing debate has become increasingly polarised.

Depending on the political lens applied, the crisis is attributed to landlords, developers, investors, planning authorities, government policy, or some combination of them all. The discussion often becomes ideological very quickly.

Yet the longer one spends working inside the housing system — acquiring sites, converting redundant buildings, regenerating property and delivering homes — the clearer a simpler explanation becomes.

Britain’s housing challenge is largely the consequence of a system that has not produced enough homes for a very long time.

When housing supply consistently falls short of demand, the outcomes are predictable. Rents rise, ownership becomes harder to access, and younger generations find it increasingly difficult to establish themselves. These pressures then feed political frustration, which in turn produces policy interventions that sometimes make the supply problem even harder to solve.

Depending on the political lens applied, the crisis is attributed to landlords, developers, investors, planning authorities, government policy, or some combination of them all. The discussion often becomes ideological very quickly.

Yet the longer one spends working inside the housing system, acquiring sites, converting redundant buildings, regenerating property and delivering homes, the clearer a simpler explanation becomes.

Britain’s housing challenge is largely the consequence of a system that has not produced enough homes for a very long time.When housing supply consistently falls short of demand, the outcomes are predictable. Rents rise, ownership becomes harder to access, and younger generations find it increasingly difficult to establish themselves. These pressures then feed political frustration, which in turn produces policy interventions that sometimes make the supply problem even harder to solve.

The debate therefore often becomes focused on redistributing the limited housing stock that already exists, rather than addressing the deeper question of how more homes are created in the first place.

Housing systems, like most economic systems, respond to incentives. When the environment encourages investment, development and regeneration, more homes are produced. When it discourages those activities, the pipeline inevitably slows.

With that in mind, I recently set out a simple Housing Supply Manifesto. It is not designed as an ideological document and it is not intended to defend any particular interest group. It is simply an attempt to outline the types of structural conditions that tend to lead to more housing being delivered.

The principles are as follows.

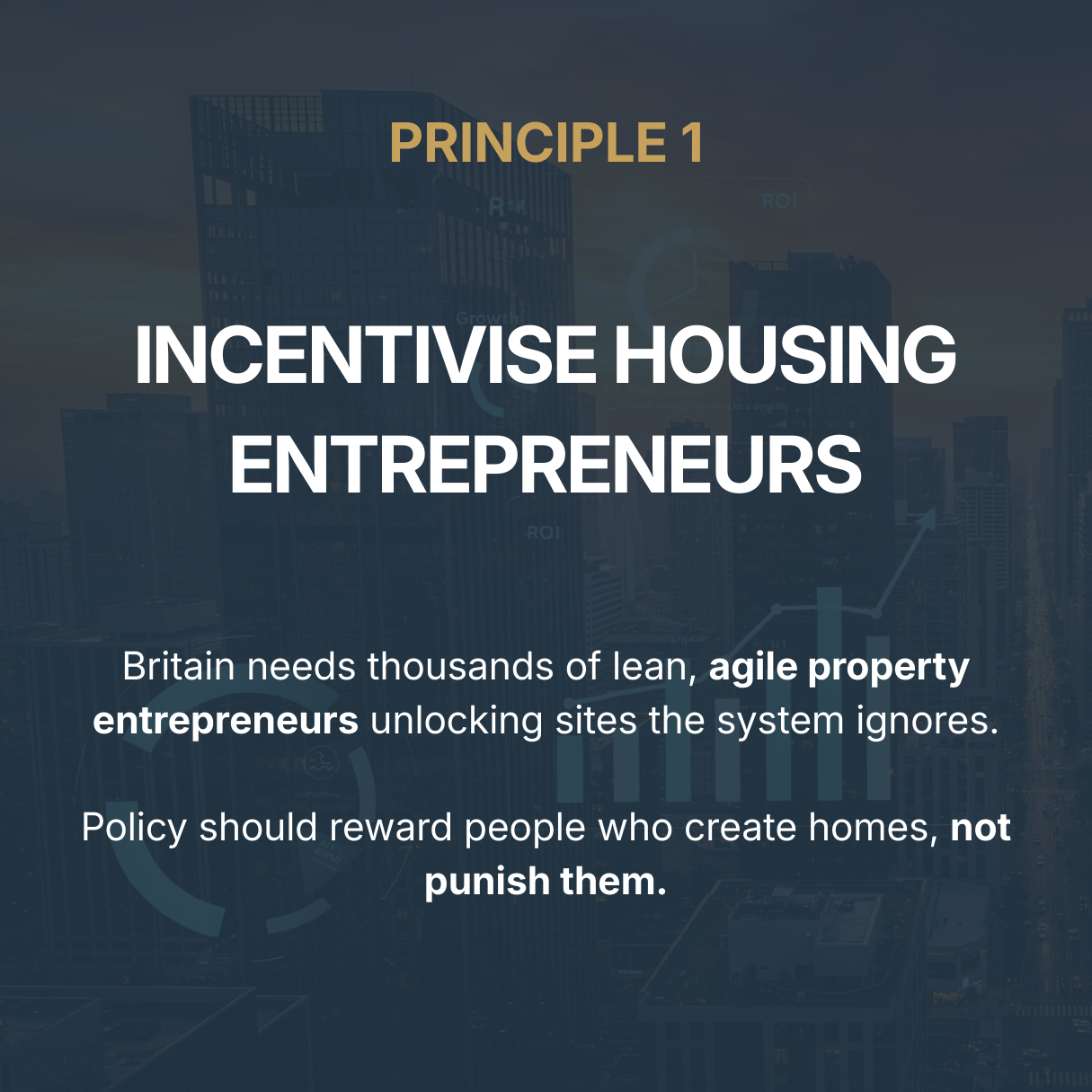

1. Incentivise the Creation of New Housing

Britain will not solve its housing shortage without private capital. Policy should actively encourage investors and developers who create new homes — whether through conversions, regeneration or new construction.

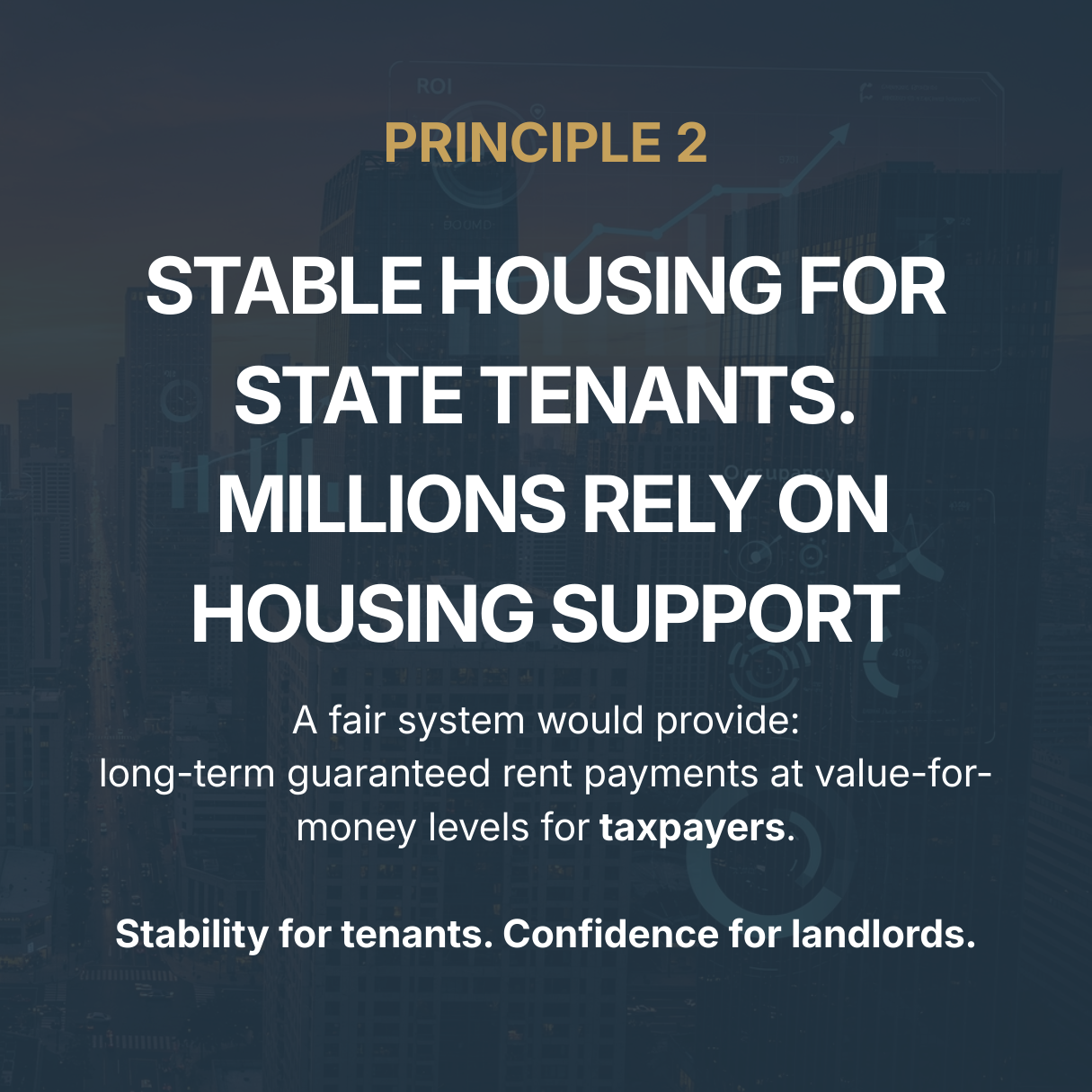

2. Provide Stable Housing for State Tenants

The private rental sector already houses millions of people who receive housing support. If the private sector is expected to play this role, the system must work properly. Government-backed tenancy models should guarantee rent payments at fair rates, giving tenants security and landlords confidence to provide homes.

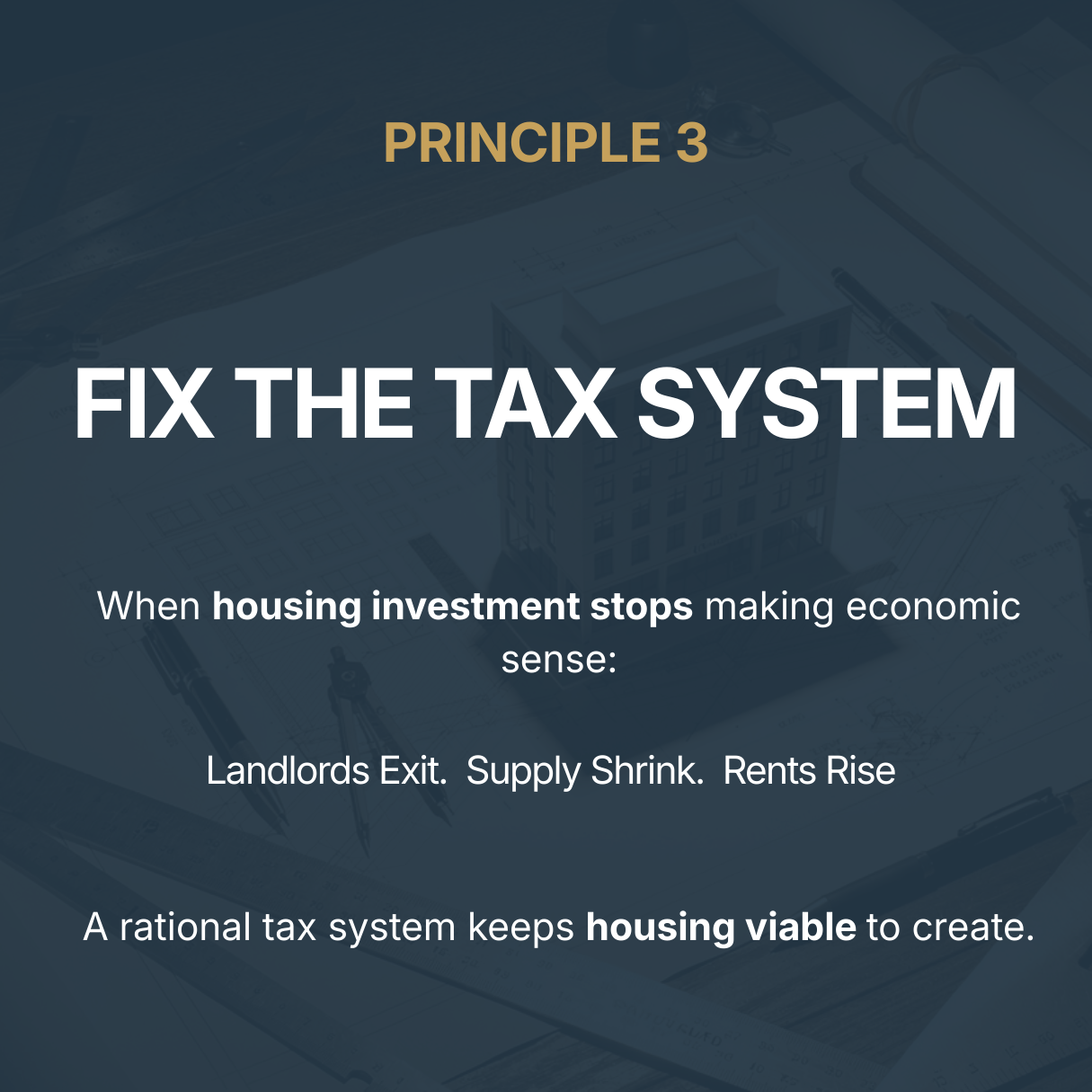

3. Reform Rental Taxation to Support Supply

The tax system should be designed so that housing investment remains viable. When landlords exit the market because taxation becomes punitive, housing supply shrinks and rents rise.

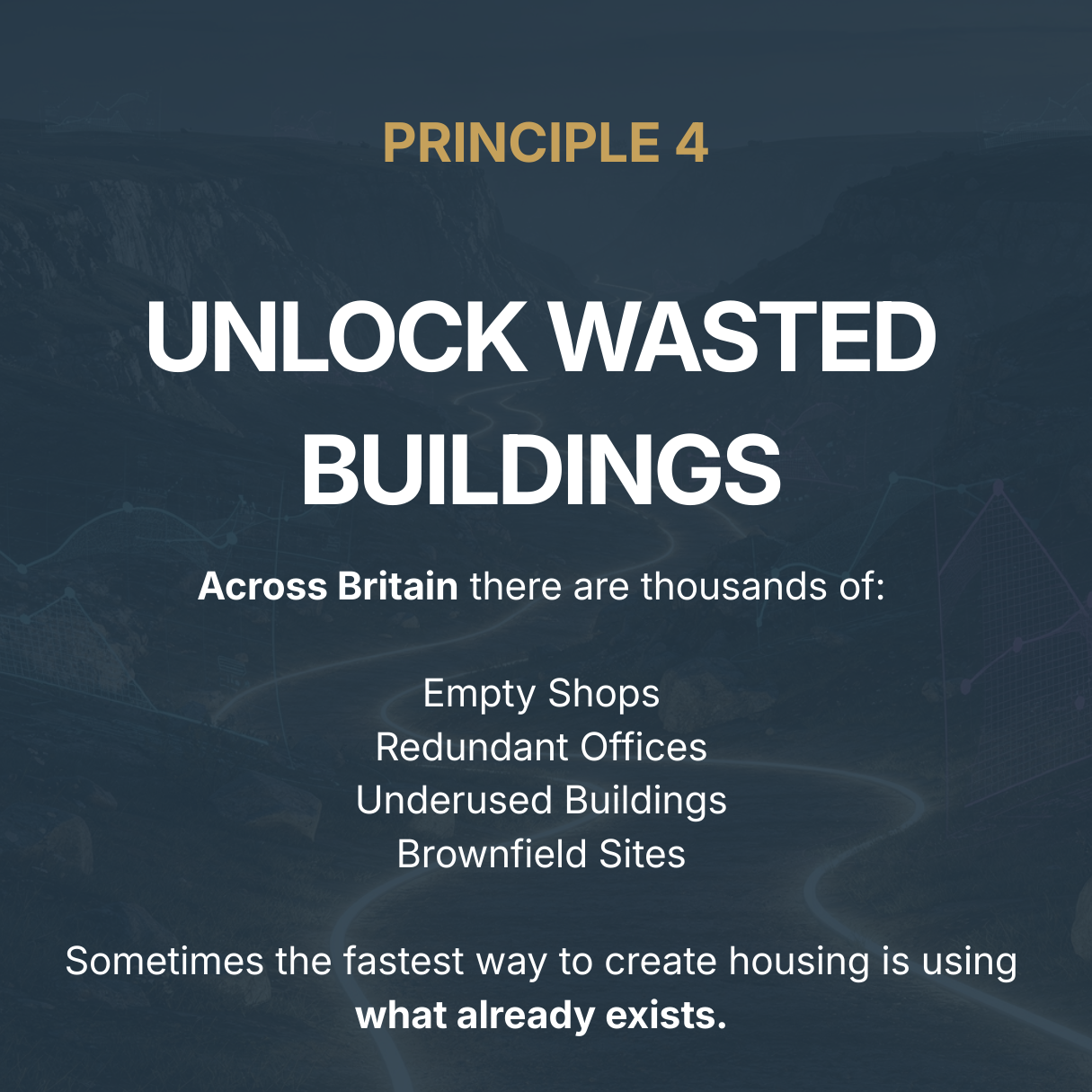

4. Unlock Wasted Buildings

Across Britain there are thousands of underused sites and redundant buildings. Regenerating these areas can create homes without expanding into green space.

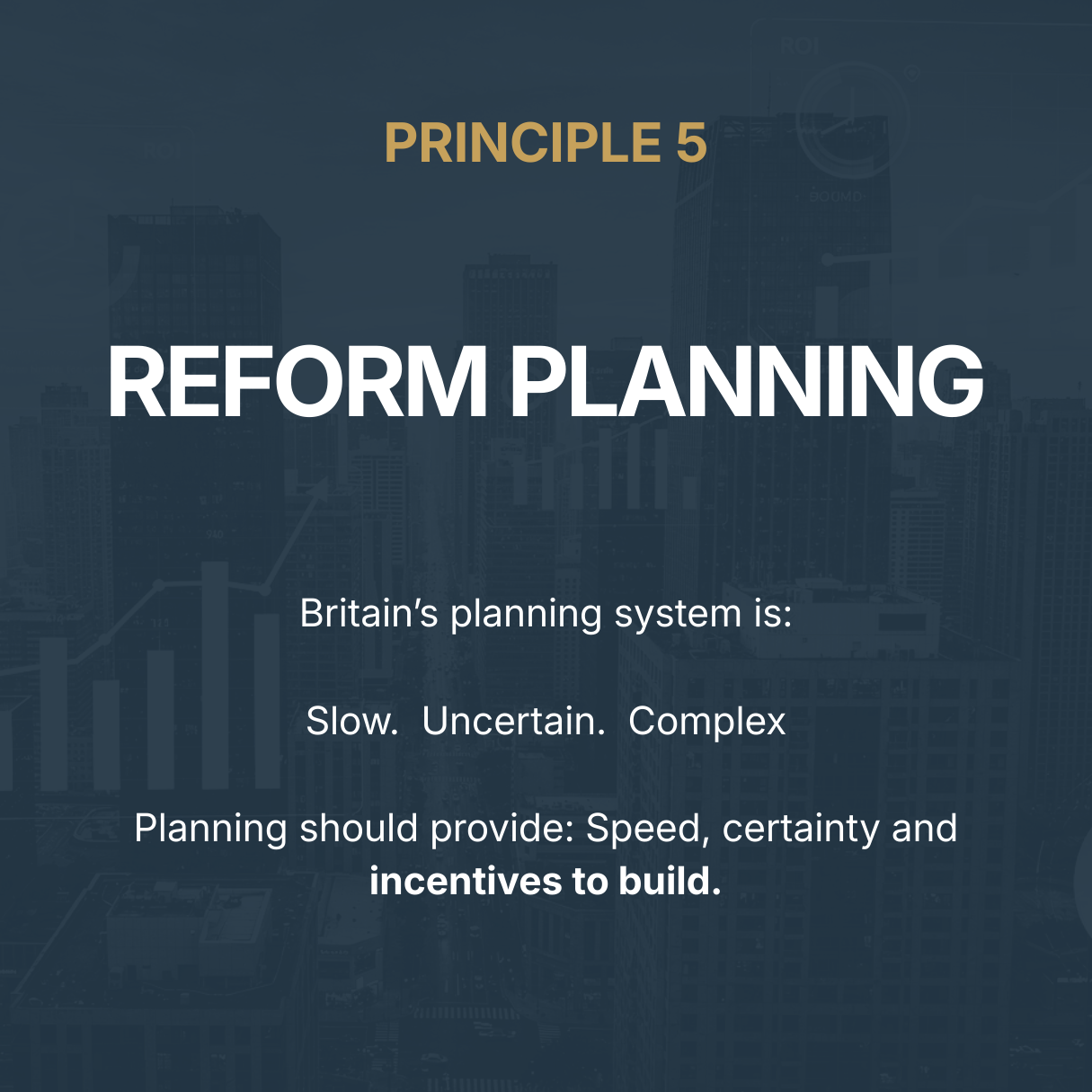

5. Create a Fast-Track Planning Route for Small Builders

Britain once built homes through thousands of small builders and local developers. Today the planning system overwhelmingly favours very large developments. A dedicated fast-track route for smaller schemes could unlock thousands of new homes that are currently stuck in bureaucracy.

6. Simplify Housing Regulation

Over time the housing system has accumulated layer upon layer of complex regulation. Simplifying these rules would reduce costs and increase the number of homes delivered.

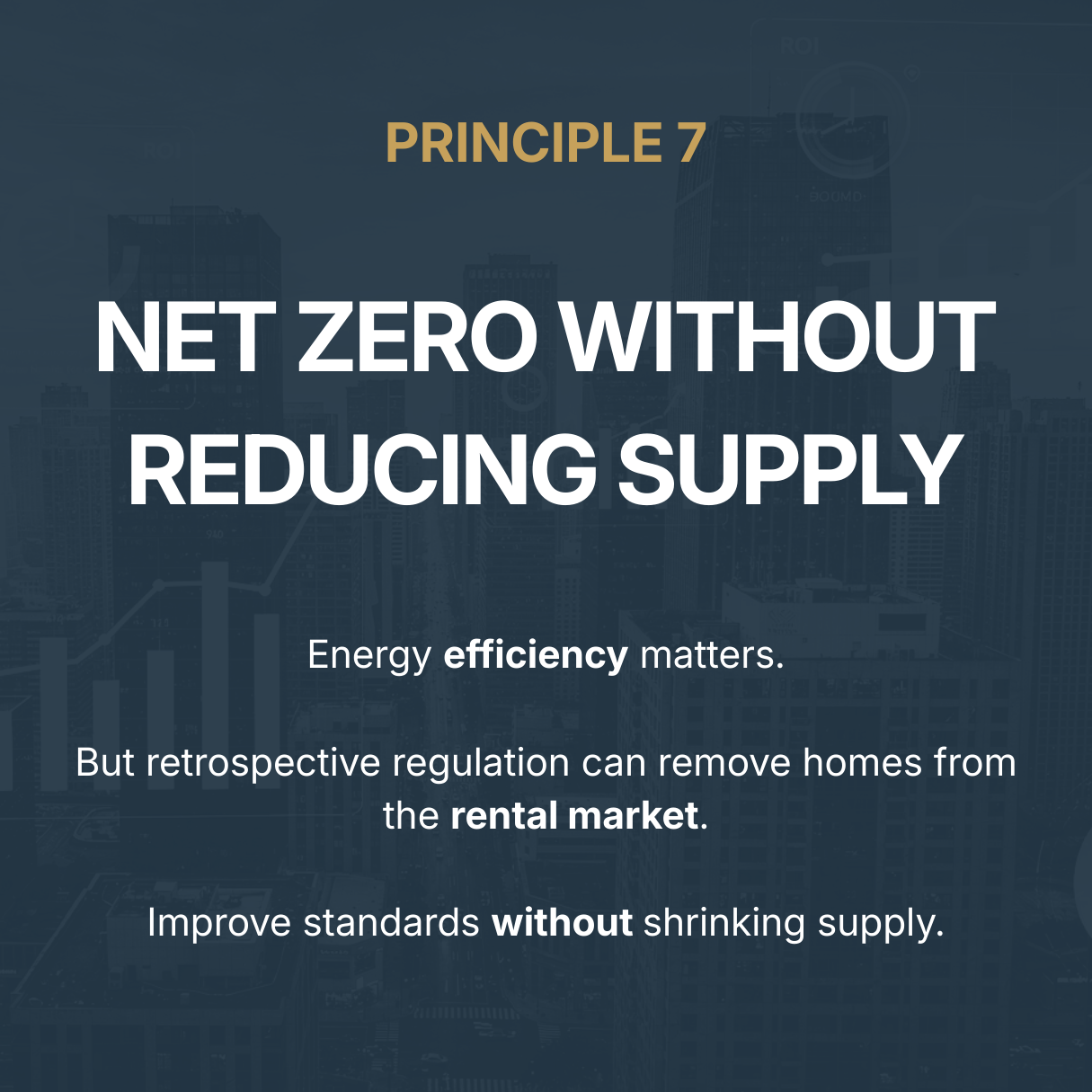

7. Transition to Net Zero Without Removing Homes From the Market

Improving the energy efficiency of Britain’s housing stock is important. But forcing sudden, expensive upgrades on existing landlords risks pushing homes out of the rental market. The transition needs realistic timelines and financing options.

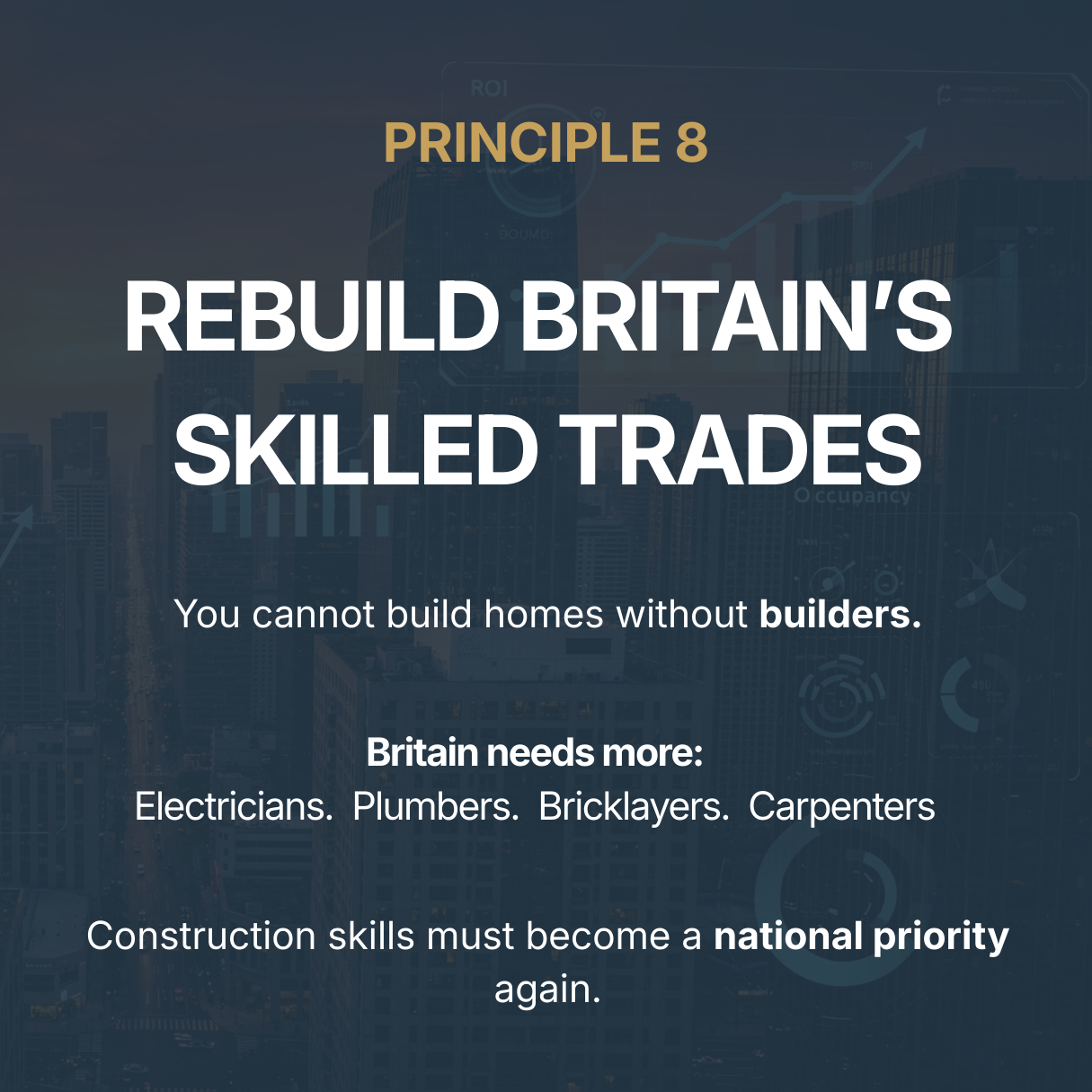

8. Rebuild the Construction Skills Pipeline

Britain cannot build more homes without skilled workers. The country needs a major expansion of trade apprenticeships, vocational training and incentives for construction careers.

9. Encourage Public–Private Housing Partnerships

Government can play an important role by assembling land, planning infrastructure and providing certainty. Private developers can then deliver housing efficiently.

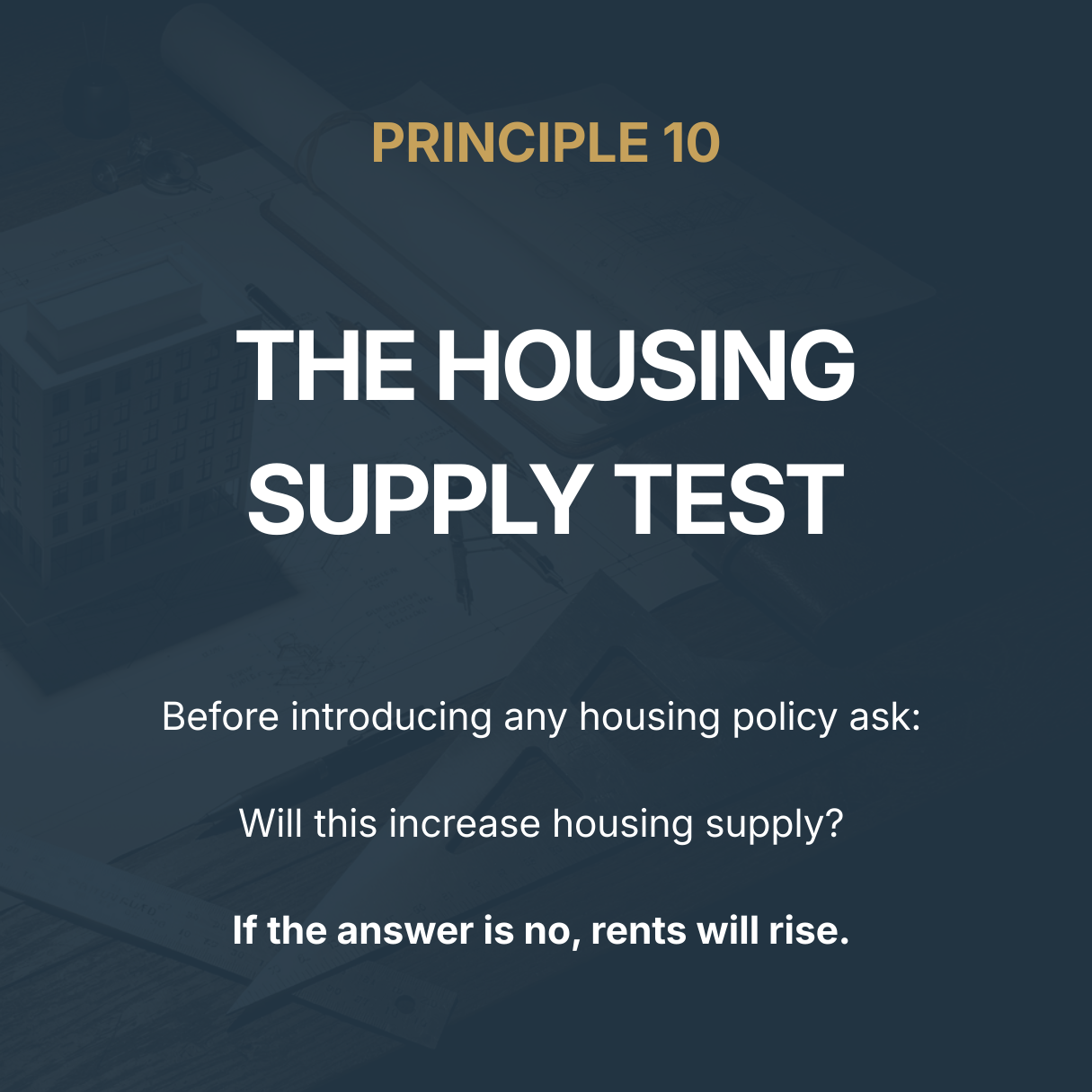

10. Introduce a Housing Supply Test for All Policy

Before introducing any new housing regulation, policymakers should ask a simple question: will this policy increase housing supply or reduce it?

Ultimately, housing policy should be judged by its outcomes rather than by the narratives that often surround it. The central test is straightforward: whether the system results in more homes being created.

A functioning housing system is not one in which different groups win arguments against each other. It is one in which the incentives align in a way that steadily increases the supply of homes available to the population.

When that happens, housing markets tend to stabilise. Renters gain greater choice, ownership becomes more attainable, and communities benefit from investment and regeneration.

In that sense, the objective is not to favour landlords, developers or tenants. It is simply to design a system that reliably produces more homes, because a country that struggles to house its population properly will ultimately struggle to prosper.

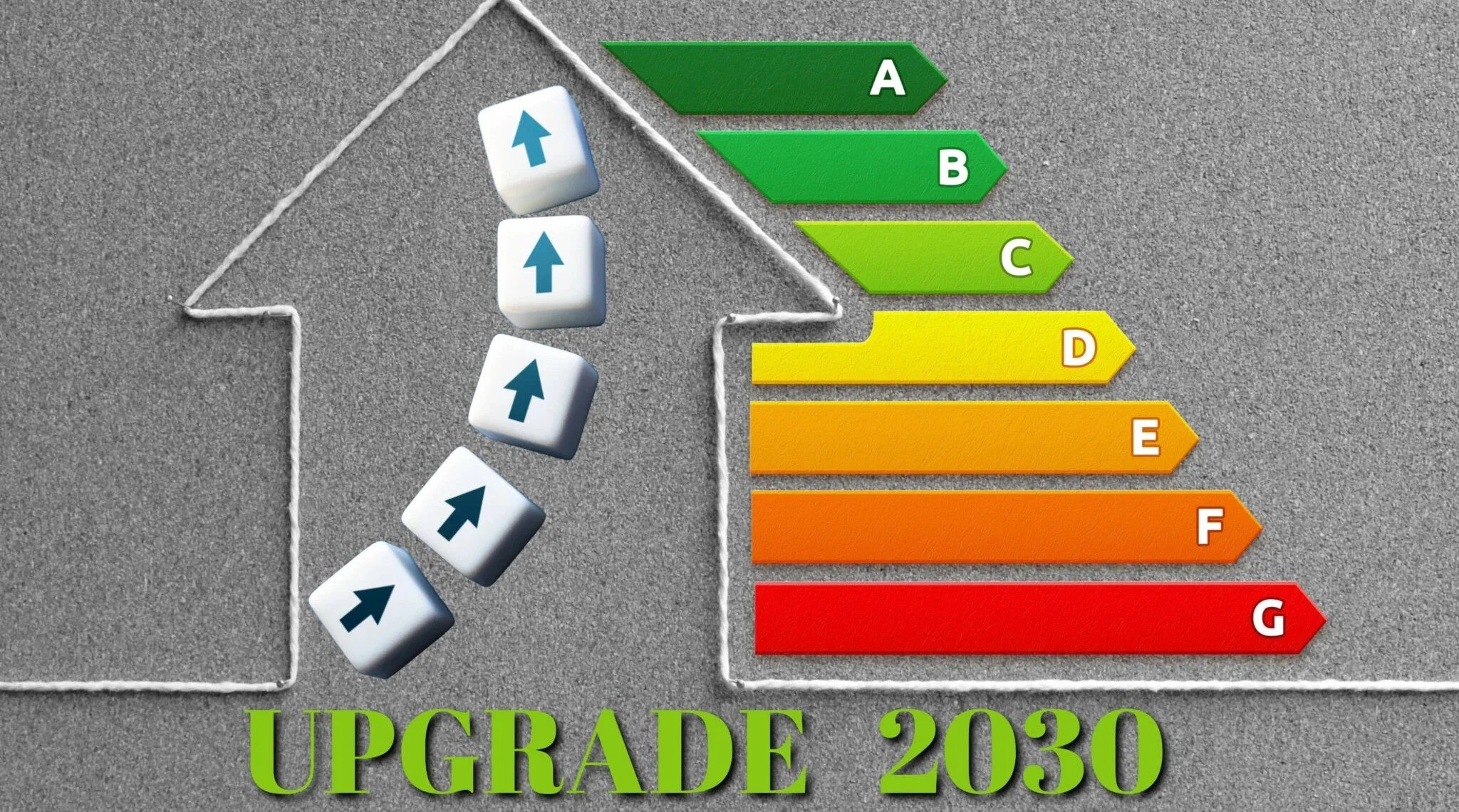

The Quiet Reshuffle of the Private Rented Sector

Why the new EPC and Decent Homes trajectory matters far more than people realise

If you take the government’s updated Decent Homes Standard and revised MEES direction at face value, and then run it forward using reasonable assumptions, you don’t get a gentle adjustment to the private rented sector.

You get a violent reshuffling.

Not an overnight collapse.

Not an apocalypse.

But a multi-year sorting mechanism that strands some stock, squeezes certain landlords out, reprices whole sub-markets, and quietly advantages those who create new, rental-grade dwellings over those trying to preserve legacy stock.

What follows is a sector-level model: Who gets squeezed, what becomes non-viable, how behaviour shifts, and why tenants ultimately sit downstream of all of it.

image from property 118

Why the new EPC and Decent Homes trajectory matters far more than people realise

If you take the government’s updated Decent Homes Standard and revised MEES direction at face value, and then run it forward using reasonable assumptions, you don’t get a gentle adjustment to the private rented sector.

You get a violent reshuffling.

Not an overnight collapse.

Not an apocalypse.

But a multi-year sorting mechanism that strands some stock, squeezes certain landlords out, reprices whole sub-markets, and quietly advantages those who create new, rental-grade dwellings over those trying to preserve legacy stock.

What follows is a sector-level model: Who gets squeezed, what becomes non-viable, how behaviour shifts, and why tenants ultimately sit downstream of all of it.

1. Why “four years” is genuinely short in housing

October 2030 sounds comfortably distant if you’re thinking politically.

It’s not distant at all in housing terms.

EPC and MEES compliance is not a cosmetic exercise. It involves:

material capex

design decisions

installer availability

tenant access and disruption

void planning

financing and re-valuation risk

Add to that a simple behavioural reality: Many landlords will not act until rules are final and enforcement feels real.

Now layer in the structure of the sector itself. A large proportion of the PRS is held by:

small landlords

one to three properties

limited balance sheets

limited appetite for repeated regulatory projects

So while the deadline is 2030, the market reaction starts much earlier.

A realistic mental model looks something like this:

2026–2027: denial / wait-and-see

2027–2028: cost discovery and early exits

2028–2029: scramble, installer bottlenecks, rising costs

2029–2030: forced decisions and accelerated disposals

By the time enforcement arrives, much of the repricing has already happened.

2. The key concept: “stranded stock”

The most important shift isn’t that the bar is being raised.

It’s that the bar itself is being rebuilt.

A fabric-first, energy-system-aware approach doesn’t just ask how efficient a home is — it asks whether it can realistically be upgraded to operate in a decarbonising system.

That creates a class of housing that is simply “hard to treat”, particularly:

solid wall terraces

flats in blocks where landlords don’t control the envelope

conservation areas with planning constraints

electrically constrained properties

awkward layouts where heat distribution and ventilation upgrades are invasive

The result is a new category in the market:

Homes that are perfectly fine to live in.

Perfectly fine to sell to an owner-occupier.

But increasingly non-viable to rent.

Historically, owner-occupier viability and rental viability overlapped heavily.

This policy pulls them apart.

That’s a structural change.

3. How landlords are likely to behave (natural assumptions)

Assume the following, none of which are extreme:

A meaningful share of PRS stock requires more than light-touch upgrades

Installer capacity tightens as deadlines approach

Costs rise non-linearly

Many landlords are already fatigued by tax, regulation, and interest rates

From there, behaviour becomes fairly predictable.

A) Early exit by small landlords

Landlords with:

low yields

older stock

limited cash reserves

are unlikely to embark on multi-stage retrofit programmes.

They sell.

Often into the owner-occupier market.

That increases sales supply — but permanently reduces rental supply, because many of those homes don’t come back into the PRS.

B) Consolidation by “capex-capable” operators

Larger or more professional landlords — those with:

project management capability

access to finance

portfolio-level planning

will buy discounted stock and upgrade it.

The outcome isn’t fewer homes.

It’s fewer landlords, holding more homes.

C) Rent pressure intensifies, even if prices soften

This is the part policymakers often underestimate.

If rental supply falls faster than demand, rents rise.

And when compliance raises operating costs, landlords who remain in the sector price that risk in.

So you can quite plausibly see:

house prices stagnating or softening in some segments

rents rising at the same time

That combination is politically awkward — but economically coherent.

4. Near-term mechanics: repricing, not a cliff edge

This isn’t a sudden ban. It’s a sorting process with a deadline.

Expect widening spreads between:

Turnkey, compliant rentals (premium pricing, high liquidity)

“Needs upgrade” stock (discounted for capex, hassle, and risk)

Hard-to-treat / exemption-reliant stock (discounted further, regulatory overhang)

Owner-occupier-only stock (priced on different fundamentals entirely)

The closer we move toward 2030, the sharper those spreads become.

That’s not collapse.

It’s stratification.

5. What tenants experience (second-order effects)

Tenants don’t experience policy through consultation documents.

They experience it through availability, price, and choice.

If we assume a net reduction in PRS supply in certain areas, tenants feel it as:

fewer listings

higher rents

tighter affordability checks

more competition

increased churn when properties are sold or taken out for upgrade

Exemptions don’t create homes.

They just delay compliance.

So the policy improves quality for some tenants …while increasing access pressure for others.

That trade-off is rarely stated explicitly.

6. Why creators of new dwellings are structurally advantaged

This is the crucial asymmetry.

If you are creating dwellings, conversions, redevelopment, net-add supply, you can:

design to the new metrics from day one

integrate fabric, heating, and energy systems properly

avoid retrofit complexity

bake compliance into funding, valuation, and exit assumptions

That is a genuine strategic advantage.

And it’s also the missing half of the policy conversation.

Standards without supply don’t raise outcomes.

They ration access.

7. Likely winners and losers by 2030

A simplified sector map looks like this:

Group Small thin-margin landlords

Likely outcome Partial exit / sell-down

Group Large professional operators

Likely outcome Consolidate + upgrade + higher rents

Group Hard-to-treat legacy stock

Likely outcome Discounted + exempted + churn

Group Turnkey compliant rentals

Likely outcome Premium pricing + strong liquidity

Group Net-new dwelling creators

Likely outcome Structural tailwind + revaluation uplift

Group Lower-income tenants

Likely outcome Higher competition + affordability pressure

This isn’t ideological.

It’s mechanical.

8. The emergence of a “rental-grade” asset class

Quietly, this policy creates a new definition of quality:

Rental-grade housing

Homes that are compliant, efficient, electrification-ready, and future-proofed.

That matters because rental-grade assets are:

easier to finance

easier to insure

easier to value

and more institutionally attractive

Over time, expect:

lenders to price future compliance risk explicitly

valuers to apply “compliance haircuts” to legacy stock

portfolios to be assessed on upgrade readiness, not just yield

This is entrepreneurial housing infrastructure in practical terms.

Not ideology.

Not virtue signalling.

Just housing designed to function as modern infrastructure, rather than patched-up legacy shelter.

Final thought

If regulation makes legacy stock harder to operate, capital must move toward creating new supply.

If it doesn’t, tenants lose.

That’s the real tension in this debate, and it’s the part we should probably be talking about far more openly.

For a deeper exploration of these ideas

including frameworks like The Unicorn Model and Creator OS, get your copy of Property Unicorns and join the movement redefining what it means to build Britain’s future.

Entrepreneurial Housing Infrastructure: The Missing Layer in Britain’s Housing System

The housing debate in Britain is stuck.

Every cycle looks the same.

Landlords versus tenants.

Private sector versus public sector.

Market failure versus state failure.

The arguments change tone, but not structure. And because the structure is wrong, the outcomes never change.

What’s missing from the conversation isn’t a better villain or a stronger policy position.

What’s missing is an entire layer of the housing system.

Britain doesn’t just have a housing crisis.

It has an infrastructure gap.

And until that gap is acknowledged and filled, no amount of political pressure, regulation, or ideological debate will fix the underlying problem.

The housing debate in Britain is stuck.

Every cycle looks the same.

Landlords versus tenants.

Private sector versus public sector.

Market failure versus state failure.

The arguments change tone, but not structure. And because the structure is wrong, the outcomes never change.

What’s missing from the conversation isn’t a better villain or a stronger policy position.

What’s missing is an entire layer of the housing system.

Britain doesn’t just have a housing crisis.

It has an infrastructure gap.

And until that gap is acknowledged and filled, no amount of political pressure, regulation, or ideological debate will fix the underlying problem.

The Two Layers We Talk About — and the One We Don’t

Most housing discussions assume the system has only two actors.

On one side, the state: social housing, planning policy, subsidies, regulation, and local authorities.

On the other, the market: volume housebuilders, institutional capital, private landlords, and developers.

These two layers are endlessly debated, criticised, and reformed. But they are also structurally limited.

The state is slow, capital-constrained, and politically reactive. Large-scale market actors are scale-dependent, planning-heavy, and optimised for return on capital, not housing adaptability.

Between these two sits a vast, under-discussed opportunity space: small-to-mid scale assets, underutilised buildings, obsolete commercial stock, fragmented ownership, and operational inefficiency.

This is where Britain’s housing system quietly fails, not because no one cares, but because no layer is explicitly responsible for fixing it.

Naming the Missing Layer: Entrepreneurial Housing Infrastructure

This is where Entrepreneurial Housing Infrastructure comes in.

Not as a slogan. Not as a political position. And not as a rebrand of buy-to-let.

Entrepreneurial housing infrastructure describes a class of activity focused on:

Repurposing underutilised or obsolete buildings

Increasing usable housing stock without competing with owner-occupiers

Creating density through design, not displacement

Delivering housing incrementally, not heroically

Improving income quality, stability, and utilisation rather than speculating on price growth

This is not rent extraction. It is not land banking. And it is not speculation disguised as “investment”.

It is infrastructure, delivered entrepreneurially because the state and large institutions are structurally unsuited to doing it at speed.

Why the Old Buy-to-Let Model Could Never Do This

Traditional buy-to-let was never designed to expand housing supply or improve system resilience.

It optimised for a completely different objective: capital appreciation over time.

Low-density residential assets, held passively, relying on external market growth, were a rational response to the conditions of the early 2000s.

But structurally, that model contributed very little to housing adaptability.

No increase in usable stock

No meaningful change in utilisation

No incentive to improve design or density

No operational innovation

Buy-to-let recycled scarcity. It didn’t expand capacity.

That doesn’t make it immoral… it makes it misaligned.

As macro conditions shifted, the model’s limitations became visible. Thin margins, fragility under volatility, tax drag, regulatory pressure, all symptoms of a structure that was never designed to function as infrastructure.

Entrepreneurial housing infrastructure is not “buy-to-let done better”. It is a different category entirely.

What These Assets Actually Contribute

When designed correctly, entrepreneurial housing assets do something quietly powerful.

They increase housing capacity without relying on:

Large-scale planning wins

Multi-year construction programmes

Competing directly with first-time buyers

Waiting for policy reform

They operate in the margins of the system — where most waste exists.

Derelict retail units.

Underused upper floors.

Fragmented mixed-use buildings.

Outdated layouts that no longer match modern demand.

By improving utilisation and income stability, these assets often house people who would otherwise be pushed into temporary accommodation, short-term rentals, or overcrowded stock. without ever entering the “social housing versus private rental” argument.

This is not charity.

It is system efficiency.

Why Speed and Smallness Matter More Than Scale

One of the great myths in housing is that bigger solutions are always better solutions.

In reality, Britain’s housing system is brittle precisely because it depends so heavily on:

Large developers

Complex planning pipelines

Long construction timelines

Entrepreneurial housing infrastructure works because it is:

Fast

Modular

Repeatable

Planning-light

Reconfiguration beats redevelopment. Operational change beats structural heroics. Incremental supply beats delayed perfection.

Speed matters because time is now one of the biggest risks in housing delivery. Capital tied up in multi-year processes is capital that cannot respond to demand shifts, cost inflation, or regulatory change.

Small, fast, repeatable interventions compound.

Slow, perfect ones stall.

A Grounded Example of the Model in Practice

Consider a mixed-use building with underutilised space, long-standing assumptions about legal or operational risk, and income that doesn’t reflect its true potential.

Under a traditional lens, it’s “too complicated”. Under an infrastructure lens, it’s mispriced.

By correcting legal misunderstandings, improving utilisation, diversifying income streams, and stabilising operations, such assets can transition from marginal to resilient, without planning dependency or displacement.

The outcome isn’t just investor return. It’s housing that exists because someone was willing to design, not wait.

That distinction matters.

Reframing the Moral Argument

Much of the housing debate is driven by moral outrage, often justified, but poorly directed.

The issue is not whether landlords are good or bad. The issue is whether capital is allocated in ways that expand housing capacity or merely extract value from scarcity.

Capital will always exist. The question is how it is structured, incentivised, and deployed.

Entrepreneurial housing infrastructure reframes the debate away from ownership morality and toward system contribution.

Not “who owns housing?” But “what does their ownership actually produce?”

The Question That Now Matters

If Britain’s housing system is broken, the most important question is no longer who to blame.

It is who is willing to design assets that actually expand the system, quickly, incrementally, and without waiting for someone else to act.

That is what entrepreneurial housing infrastructure represents.

Not a rebellion. Not an ideology. An overdue layer in a system that has been missing it for far too long.

For a deeper exploration of these ideas

including frameworks like The Unicorn Model and Creator OS, get your copy of Property Unicorns and join the movement redefining what it means to build Britain’s future.

How I Would Invest in Property in 2026 and Beyond

How I Would Invest in Property in 2026 and Beyond

(And why most people won’t)

Every property cycle creates its own myths.

In the last one, the myth was simple:

Buy a house. Add leverage. Wait.

That worked .. not because it was smart, but because the system rewarded passivity.

That era is over.

Not temporarily.

Structurally.

So when people ask me “Is property still worth investing in?” my answer is always the same:

Yes, but only if you play a different game.

If I were starting today, or rebuilding a portfolio for 2026 and beyond, I would follow five rules. Miss one, and the model eventually breaks.

(And why most people won’t)

Every property cycle creates its own myths.

In the last one, the myth was simple:

Buy a house. Add leverage. Wait.

That worked, not because it was smart, but because the system rewarded passivity.

That era is over.

Not temporarily.

Structurally.

So when people ask me “Is property still worth investing in?” my answer is always the same:

Yes… but only if you play a different game.

If I were starting today, or rebuilding a portfolio for 2026 and beyond, I would follow five rules. Miss one, and the model eventually breaks.

Rob Stewart Property

Rule 1: Passive appreciation is dead — value must be forced

The biggest mistake investors make is assuming accumulation phases reward patience.

They don’t.

They reward intervention.

In real terms, UK house prices have already corrected hard since interest rates rose. That doesn’t mean prices crash, it means time and inflation do the work while capital sits idle.

If your strategy relies on:

“Long-term growth”

“Rent inflation”

“The market coming back”

You’re not investing.

You’re waiting.

Every asset I would buy must have forced appreciation built in:

Change of use

Density uplift

Reconfiguration

Tenure transformation

Operational enhancement

If the value only goes up if the market rescues it, the deal is invalid.

Rule 2: Cashflow must be engineered through density — not leverage

Debt used to hide bad models.

It doesn’t anymore.

Low-density assets collapse under:

Higher interest rates

Void risk

Tax drag

Regulation

The new rule is simple:

Density is the new leverage.

Cashflow must be created inside the asset, not borrowed from the bank.

That means:

Multiple income lines per title

Income spread across users, not tenants

Assets that still work when rates stay higher for longer

If one tenant leaving breaks the model, the model is fragile.

I would only buy assets where cashflow is designed, not assumed.

Rule 3: Tax is a design variable — not an afterthought

“Just buy it in a limited company” is entry-level thinking.

Tax efficiency isn’t a structure problem.

It’s an asset selection problem.

What you buy determines:

How income is taxed

Whether allowances apply

How capital is treated

What exits are available

In 2026 and beyond, ignoring tax at acquisition is fatal.

I would actively look for:

Commercial vs residential arbitrage

Mixed-use advantages

Capital allowances

Structures & Buildings Allowance

Stamp duty efficiency

If tax efficiency relies on “sorting it later”, it will never be sorted.

Rule 4: Assets must be net contributors to housing supply

This is where ideology breaks.

The future is not about competing with first-time buyers for family homes.

That’s lazy capital.

The only models that survive politically and economically are those that expand usable housing stock:

Repurposing obsolete buildings

Converting underutilised commercial space

Creating housing types the open market doesn’t supply

Increasing density without sprawl

These assets don’t extract from the system.

They repair it.

And crucially — they attract capital when policy tightens elsewhere.

Rob Stewart Property

Rule 5: Speed beats perfection — time is the hidden risk

The biggest killer of returns in the next decade won’t be price.

It will be time.

Planning delays.

Construction inflation.

Multi-year timelines.

The old belief was:

Bigger projects = bigger rewards.

The new reality is:

Planning is broken

Build costs are volatile

Time magnifies every risk variable

I would favour:

Planning-light strategies

Reconfiguration over redevelopment

Operational change over structural change

Assets that move fast, not heroically

If a deal only works “once completed”, it’s already in trouble.

The uncomfortable conclusion

Most people will sit out this phase waiting for clarity.

Institutions won’t.

They’ll accumulate assets that:

Work in flat markets

Survive hostile policy

Compound when confidence returns

By the time sentiment flips, the best assets won’t be available.

They’ll already be owned.

Quietly built during the years everyone else spent arguing.

For a deeper exploration of these ideas

including frameworks like The Unicorn Model and Creator OS, get your copy of Property Unicorns and join the movement redefining what it means to build Britain’s future.

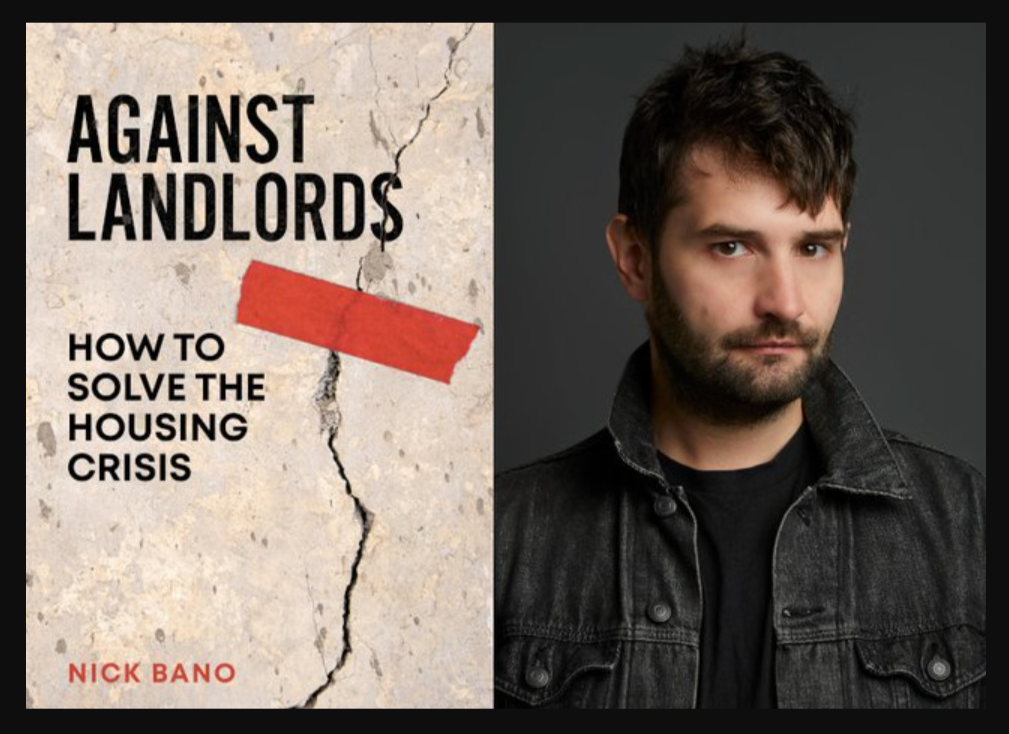

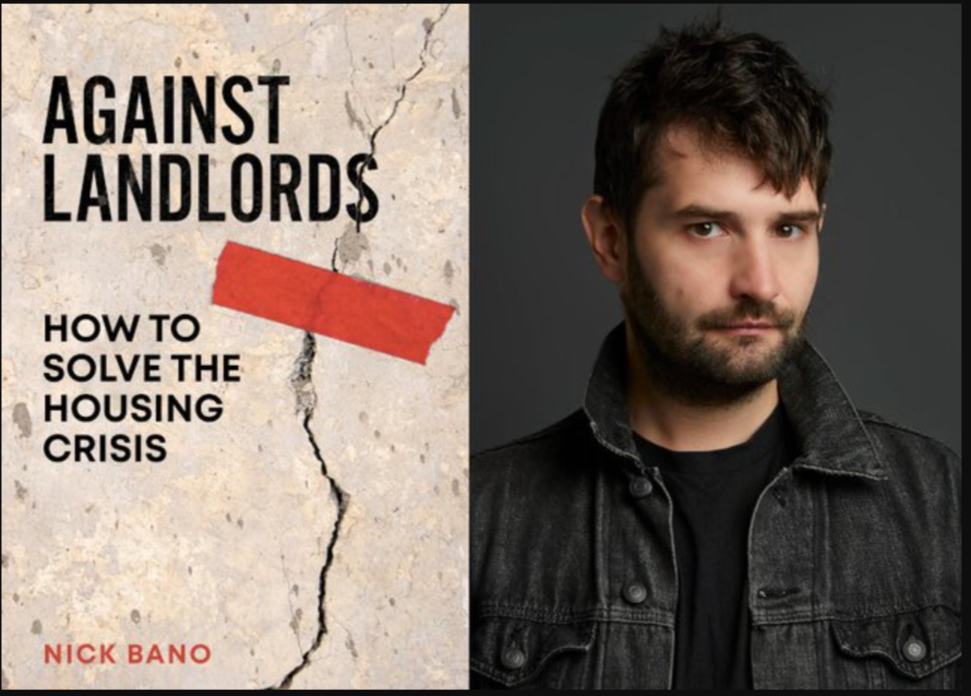

Why “Abolishing Landlords” Is an Ideological Claim, Not a Housing Solution

A critical analysis of Nick Bano’s argument on housing, supply, and affordability

In recent debates on housing, a familiar argument has resurfaced with renewed confidence: that Britain does not suffer from a housing shortage, but from “landlordism”. The claim is that abolishing or collapsing the private rented sector would restore affordability, security, and social justice… without the need for large-scale housebuilding.

This view is most clearly articulated by Nick Bano, a barrister specialising in renters’ rights and the author of Against Landlords. His Guardian essay has become a reference point for many online commentators, particularly those using terms such as “rentier economy” or “landlordism” as explanatory frameworks for the housing crisis.

The problem is not that this argument raises moral concerns… it does.

The problem is that it mistakes a complex systems failure for a simple class conflict, and in doing so replaces housing economics with ideology.

This article examines why.

A critical analysis of Nick Bano’s argument on housing, supply, and affordability

In recent debates on housing, a familiar argument has resurfaced with renewed confidence: that Britain does not suffer from a housing shortage, but from “landlordism”. The claim is that abolishing or collapsing the private rented sector would restore affordability, security, and social justice… without the need for large-scale housebuilding.

This view is most clearly articulated by Nick Bano, a barrister specialising in renters’ rights and the author of Against Landlords. His Guardian essay has become a reference point for many online commentators, particularly those using terms such as “rentier economy” or “landlordism” as explanatory frameworks for the housing crisis.

The problem is not that this argument raises moral concerns… it does.

The problem is that it mistakes a complex systems failure for a simple class conflict, and in doing so replaces housing economics with ideology.

This article examines why.

Nick Bano’s argument on housing, supply, and affordability

1. The central claim: no housing shortage, only a landlord problem

Bano’s core thesis is straightforward:

Britain has enough homes per capita compared to other OECD countries

Housing affordability has worsened despite a net increase in housing stock

Therefore, supply is not the issue

The true cause of the crisis is the private rented sector and the extraction of rent

If this claim holds, then policies focused on building more homes are misguided, and the solution lies in de-commodifying housing by driving landlords out.

Everything else in the argument depends on this logic.

Unfortunately, it does not survive scrutiny.

2. The misuse of “homes per capita”

The most significant analytical flaw is the reliance on national homes-per-capita averages as evidence that Britain does not face a supply problem.

Housing markets do not function nationally. They function locally.

A surplus of homes in one region does not relieve shortages in another. Vacant properties in declining or low-demand areas do not house workers, families, or key staff in high-productivity cities. London, Oxford, Cambridge, Bristol, Manchester and parts of the South East face acute shortages regardless of national averages.

Moreover, “homes per capita” ignores household formation, which is the real driver of demand:

More single-person households

Later family formation

Higher divorce and separation rates

Longer life expectancy

Increased labour mobility

All of these increase demand for units even if population growth is flat.

This is not a marginal oversight. It is a fundamental misunderstanding of how housing demand works.

3. Affordability vs supply is a false dichotomy

Bano repeatedly frames the debate as affordability versus supply, as if the two are unrelated.

They are not.

Affordability is an outcome of:

supply

location

income

finance costs

regulation

and expectations

Countries and cities that have stabilised rents over time have done so by overwhelming demand with supply, not by suppressing ownership structures.

To argue that supply “cannot” matter because prices remain high is to confuse insufficient supply with constrained supply. In the UK, planning risk, finance costs, land banking incentives, and infrastructure bottlenecks all restrict new development — particularly where demand is strongest.

Blaming landlords for outcomes produced by these constraints is analytically convenient, but incomplete.

4. The romanticisation of the 1970s private rented sector collapse

A key historical reference point in Bano’s argument is the collapse of the private rented sector in the mid-20th century, which he presents as evidence that reducing landlord participation improves affordability.

What is missing is context.

That period coincided with:

full employment

strong wage growth

defined-benefit pensions

cheap public borrowing

mass council housebuilding

lower household mobility

a radically different demographic profile

Municipalisation succeeded because the state had both the financial capacity and the political consensus to absorb housing stock as private capital exited.

Today, councils are capital-constrained, borrowing is expensive, construction capacity is limited, and political consensus is fractured. Attempting to recreate 1970s outcomes without 1970s conditions is not policy — it is nostalgia.

5. The Vienna comparison — selectively applied

Vienna is frequently cited as proof that landlord-light or landlord-free systems produce superior housing outcomes.

But Vienna was not created by abolishing landlords.

It was created through:

a century of continuous public investment

aggressive, large-scale housebuilding

deep, ongoing subsidies

long-term rent regulation tied to abundant supply

private developers operating within a heavily structured system

Crucially, Vienna did not oppose building. It built relentlessly.

To cite Vienna while opposing large-scale construction is to extract the aesthetic of the model while rejecting its foundations.

6. The straw-man view of developers and supply

Bano dismisses the idea that increasing supply could reduce prices by suggesting developers would never build enough homes to devalue their assets.

This misunderstands how markets function.

Markets do not require altruism. They respond to margins. When marginal profit declines, land values compress, speculative returns fall, and price growth slows or stabilises relative to wages.

No serious housing economist argues that developers will build until prices collapse, only that constrained supply guarantees scarcity rents.

Rejecting supply because it offends an ideological narrative does not protect renters. It entrenches the very scarcity that makes rents punitive.

7. The missing analysis: consequences of landlord abolition

Perhaps the most telling omission in Bano’s argument is the absence of transitional analysis.

If landlords are abolished or forced out:

Who funds repairs and maintenance during the transition?

Who finances new housing while asset values are falling?

What happens to renters during forced sell-offs?

Who absorbs the losses — banks, pension funds, councils, taxpayers?

How is capital flight prevented?

These questions are not technicalities. They are decisive.

Housing is capital-intensive. Removing private capital without a fully funded, politically viable replacement does not liberate renters — it reduces supply, freezes mobility, and raises risk premiums.

The first people harmed would not be landlords.

They would be renters.

8. When economics becomes moral theatre

The repeated use of terms such as “landlordism” and “rentier economy” signals a shift from analysis to moral positioning.

Once housing is framed primarily as a struggle against a villainous class, trade-offs disappear, incentives are ignored, and outcomes become secondary to virtue.

Housing crises are not solved by identifying enemies. They are solved by systems design.

Every country that has made sustained progress on affordability has done two things simultaneously:

built aggressively

regulated sensibly

None have abolished landlords.

9. A more serious starting point

None of this is a defence of poor standards, insecurity, or exploitation in the private rented sector. Reform is necessary. Regulation is overdue.

But serious reform starts with understanding mechanisms, not slogans.

The housing crisis is real.

Renters are under pressure.

The status quo is failing.

Replacing economics with ideology will not fix that.

It will make it worse.

-Rob Stewart

For a deeper exploration of these ideas

including frameworks like The Unicorn Model and Creator OS, get your copy of Property Unicorns and join the movement redefining what it means to build Britain’s future.

Tenants and small landlords are not natural enemies.

Congratulations. You fell for it.

If the reaction to my Social Media Posts demonstrated anything, it is that the system remains remarkably effective at doing exactly what it was designed to do. With impressive efficiency, it split the country into familiar, warring camps: landlords versus tenants, rich versus poor, parasites versus victims. The lines were drawn, the moral positions assumed, and the arguments duly rehearsed.

Congratulations. You fell for it.

If the reaction to my Social Media Posts demonstrated anything, it is that the system remains remarkably effective at doing exactly what it was designed to do. With impressive efficiency, it split the country into familiar, warring camps: landlords versus tenants, rich versus poor, parasites versus victims. The lines were drawn, the moral positions assumed, and the arguments duly rehearsed.

This, in practice, is what divide and conquer looks like.

Because while public attention is absorbed by online skirmishes, something far more consequential is unfolding with very little scrutiny. The fury directed at small, individual landlords has created the perfect distraction from a much larger structural shift taking place beneath the surface of the housing market.

“Ron and Marge”, the archetypal couple with two rental properties purchased over decades of work and saving, have become convenient symbols of everything that is supposedly wrong with the system. They are accused of hoarding, profiteering, and moral failure. They are presented as the villains in a housing crisis they did not create.

They are not, in fact, the problem.

“Ron and Marge” are not draining the state…

Nor are they engaged in some predatory scheme. They are ordinary people who responded rationally to the incentives and warnings of successive governments: that the pension system was unreliable, that personal provision was essential, and that property represented security in an increasingly uncertain economy.

While public anger is channelled towards people like them, institutional investors, international conglomerates, and pension funds are acquiring housing stock at scale. Not two properties, but thousands. Entire developments. Whole neighbourhoods.

This transfer is not loud or theatrical. It does not trend on social media. It happens through transactions, balance sheets, and long-term capital strategies. By the time it becomes visible, it is usually irreversible.

It is worth stating plainly what is so often overlooked. Most tenants would be better off renting from Ron and Marge than from an asset management firm operating at arm’s length from the communities in which it owns homes.

Individual landlords can exercise discretion.

They can listen, adapt, and make judgments based on human circumstances. An institution cannot do this in any meaningful sense. Its obligations are contractual and fiduciary, not relational. Decisions are shaped by policy, not empathy, and exceptions are liabilities rather than virtues.

Calls to eliminate small landlords often ignore where housing ownership flows once those landlords exit the market. Properties do not disappear. Demand does not evaporate. Instead, homes are consolidated into larger portfolios, increasingly controlled by organisations whose primary duty is to maximise yield for distant investors.

This concentration of ownership should concern anyone serious about affordability, stability, or social cohesion. History offers little comfort when essential goods become dominated by a small number of powerful actors. Choice diminishes, prices harden, and accountability becomes abstract.

The prevailing narrative, however, remains stubbornly simplistic. Housing debates are reduced to moral binaries that generate heat but little clarity. Landlords are cast as inherently exploitative, tenants as inherently virtuous. Structural failures are personalised, and systemic incentives are ignored.

Outrage, after all, is politically useful. It mobilises emotion, fragments solidarity, and keeps attention focused laterally rather than vertically.

Over the past decade, regulatory and tax pressures have steadily increased on small landlords. Each measure is often defensible in isolation, but together they form an environment that many individuals find unsustainable. Those without scale, legal teams, or access to cheap capital are the first to leave.

The question is not whether landlords should be regulated. They should be. The question is who regulation ultimately advantages. In practice, complexity and compliance favour large institutions far more than individuals.

At the heart of the housing crisis lies a basic arithmetic problem. There are not enough homes.

This is not resolved by reallocating blame or by shrinking the pool of people willing to provide rental accommodation. Fewer landlords do not mean lower rents. They mean fewer options, greater concentration, and more power in fewer hands.

Most landlords are not property magnates

They are participants in a system that increasingly requires individuals to secure their own financial futures. They took risks, delayed consumption, and invested in an asset class long promoted as prudent and responsible.

At the same time, institutional ownership is frequently framed as more professional or efficient. These terms deserve scrutiny. Professional for whom? Efficient to what end?

Efficiency in this context often means treating housing purely as a financial instrument. Homes become units of yield, detached from place, community, and long-term stewardship. Decisions are optimised for return, not resilience.

None of this is an argument against tenants, who largely want what most people want: security, fairness, and a decent place to live. Nor is it an argument against reform. The current system is failing too many people to defend complacently.

What it is, however, is a warning against allowing a false conflict to obscure a genuine and accelerating shift in ownership.

Tenants and small landlords are not natural enemies. In many respects, their interests align more closely than either group’s interests align with those of global capital.

There is still time to change course. But that window is narrowing.

If housing continues to be fully financialised, control will not easily return to local hands. Once ownership is consolidated, it is rarely unwound. Communities do not regain leverage simply by recognising the mistake after the fact.

A functional housing system requires more supply, not less

More builders, not fewer. More responsible owners willing to commit capital and time to long-term provision.

It requires more net contributors to the system, not policies that inadvertently expel them.

If the aim is to stabilise rents, protect tenants, and preserve mixed communities, then attention must shift from scapegoats to structures.

The alternative is to continue applauding the spectacle while the substance quietly changes hands.

The system would prefer that debate remain fixed on Ron and Marge. It is far less comfortable when the conversation turns to who is actually accumulating the nation’s housing stock, and to what end.

Are Landlords Parasites, or the Only Reason Millions Have Homes?

Few ideas travel faster online than the claim that landlords are parasites. It is a neat moral judgement, compact enough to fit on a placard or into a tweet, and expansive enough to absorb a wide range of social frustrations. Rising rents, insecure tenancies, visible inequality, and decades of housing failure all collapse into a single villain.

The problem is not that this critique exists. The problem is that it often stops at accusation.

I want to take the argument seriously, including its strongest counterclaims, because housing is too important to be reduced to slogans. If landlords truly are parasitic, then we should be able to explain not only why they are morally wrong, but how their removal would materially improve housing outcomes.

A critical examination of housing, power, and uncomfortable trade-offs

By Rob Stewart.

Few ideas travel faster online than the claim that landlords are parasites. It is a neat moral judgement, compact enough to fit on a placard or into a tweet, and expansive enough to absorb a wide range of social frustrations. Rising rents, insecure tenancies, visible inequality, and decades of housing failure all collapse into a single villain.

The problem is not that this critique exists. The problem is that it often stops at accusation.

I want to take the argument seriously, including its strongest counterclaims, because housing is too important to be reduced to slogans. If landlords truly are parasitic, then we should be able to explain not only why they are morally wrong, but how their removal would materially improve housing outcomes.

I have been investing in and operating residential property since 2010. Over that time, I have housed somewhere between 200 and 300 people across working families, vulnerable tenants, housing benefit recipients, professionals, and elderly tenants. This does not make me neutral. It does, however, mean I have seen how policy, economics, and human behaviour interact on the ground.

So let us begin with the most common counterarguments, presented fairly, and then examine where they hold and where they collapse.

Counterargument One: “Housing Is a Human Right, Therefore It Should Not Be a Commodity”

This is the moral cornerstone of the anti-landlord position. Housing, like healthcare or education, is framed as a basic human right. From this perspective, the existence of profit in housing is itself unethical.

I agree with the premise more than critics expect. Shelter matters. Stability matters. No one should be made homeless because of speculative excess or regulatory neglect.

But recognising housing as a human necessity does not answer the operational question of provision.

Food is also a human necessity. So is energy. So is transport. In each case, the state regulates, subsidises, and intervenes, but does not directly provide all supply. Markets exist not because society is cruel, but because scale, speed, and capital are required.

In the UK, the state made a long-term political decision not to build sufficient housing itself. Social housing stock has declined steadily since the 1980s through Right to Buy, underinvestment, and demographic pressure. That decision created a vacuum.

Private landlords did not force that vacuum into existence. They moved into it. Calling housing a human right does not magically generate units. It does not summon builders, materials, planning consent, or capital. Rights require infrastructure. Infrastructure requires funding, labour, and risk-bearing.

Until critics can explain how millions of homes will be built, maintained, and allocated in the absence of private capital, the moral claim remains incomplete.

Counterargument Two: “Landlords Drive Up Prices and Rents”

This argument is more empirical and deserves careful handling. The claim is that landlords outbid first-time buyers, restrict supply, and then charge increasingly unaffordable rents.

There is some truth here, but it is context-dependent.

In high-demand, low-supply areas, competition for housing is intense. Landlords are one set of actors within that competition. However, they are not the only ones. Developers, owner-occupiers, overseas buyers, institutional funds, and pension vehicles all play a role.

The deeper driver of price inflation is chronic undersupply. The UK has failed to build enough homes for decades. When demand consistently outstrips supply, prices rise regardless of who owns the stock.

Blaming landlords for high rents without addressing planning constraints, slow delivery, labour shortages, and infrastructure bottlenecks is like blaming shopkeepers for food prices during a famine.

If landlords were the primary cause of rising rents, removing them would lower rents. In practice, when landlords exit markets, rents often rise faster due to reduced availability.

This is not ideology. It is observed behaviour.

Counterargument Three: “Landlords Add No Value and Extract Rent”

This is perhaps the most emotionally resonant claim. The landlord is framed as someone who does nothing productive, yet siphons income from tenants who work.

This caricature ignores both capital provision and ongoing operational risk.

Before a tenant moves in, a landlord typically commits tens of thousands of pounds in deposit, purchase costs, refurbishment, and compliance. That capital could have been deployed elsewhere. It is locked into a single illiquid asset.

Once the tenant is in place, the landlord carries responsibility for maintenance, safety compliance, financing risk, regulatory change, and tenant default. When things go wrong, losses are not capped.

As I write this, I am dealing with a flat that has been severely damaged by a family tenant. The deposit available to offset the damage is £550. The real cost exceeds £7,000, excluding lost rent, ongoing mortgage payments, and council tax.

This is not rare. It is routine.

The idea that landlords “add no value” assumes that housing would otherwise exist in the same form, at the same standard, without their involvement. That assumption is unproven.

Counterargument Four: “If Landlords Left, the State Would Step In”

This is the most consequential claim, and the one least supported by evidence.

Local authorities are already under severe financial pressure. Temporary accommodation costs councils billions each year. Social housing waiting lists are at record levels. Construction capacity is constrained by labour shortages and planning delays.

Even if the political will existed to massively expand state-built housing, it would take years, likely decades, to deliver at scale.

In the meantime, people still need somewhere to live.

When private rental supply contracts, the immediate outcomes are not mass rehousing by councils. They are overcrowding, family displacement, hotel use, and homelessness.

This is not a hypothetical scenario. It is already visible in areas where rental supply has tightened.

Counterargument Five: “Good Landlords Are the Exception”

Another common response is that while some landlords may behave ethically, they are outliers within a fundamentally exploitative system.

This argument collapses individual behaviour into structural critique. It assumes intent where constraint is often the driver.

Most landlords I know are not maximising profit. They are responding to rising costs, regulatory shifts, and financing pressures. Labour costs have risen sharply. Materials are more expensive. Tax treatment has worsened. Interest rates have changed the viability of marginal stock.

Legacy rents often lag far behind market rates. In one of my buildings, an elderly tenant has lived there since 1990. Market rent would be close to £900. I charge £550. Not because I am forced to, but because stability matters and displacement would be unjust.

This does not make me heroic. It makes me typical of long-term landlords who value continuity over churn.

Eviction, contrary to popular belief, is rarely a strategy. It is expensive, slow, and emotionally draining. It is usually a last resort after sustained arrears and failed engagement.

Counterargument Six: “Landlords Are Withholding Housing From Ownership”

This argument claims that renters would all prefer to buy, and that landlords prevent this by hoarding stock.

The reality is more complex.

Not everyone wants to buy. Not everyone can. Short-term workers, mobile professionals, students, and people recovering from financial shocks often need flexibility, not a mortgage.

A functioning housing system requires a rental sector. The question is not whether renting should exist, but how it should be regulated and balanced.

Removing landlords does not automatically convert renters into homeowners. It often converts renters into more precarious renters.

The Structural Failure We Keep Avoiding

Many critiques of landlords are emotionally understandable because they are responding to real pain. Housing insecurity is destabilising. High rents limit life choices. Poor standards damage trust.

But misidentifying the cause leads to ineffective solutions.

The core failure is not the existence of landlords. It is the persistent under-delivery of housing at every level, combined with policy that simultaneously relies on private provision and punishes it.

Housing has been turned into a moral battleground when it should be treated as infrastructure.

Infrastructure requires long-term thinking, mixed provision, and uncomfortable trade-offs. It requires acknowledging that no single actor, public or private, can carry the entire burden alone.

Where This Leaves Us

You can hate the system. I understand that impulse.

But removing landlords does not replace housing. It removes supply.

Until there is a credible, funded, and time-bound plan to build and maintain millions of additional homes, private landlords remain part of the scaffolding holding the system up. That does not mean the system should not change. It does mean change must engage with reality, not fantasy.

So I return to the question that critics rarely answer: If private landlords disappeared tomorrow, where would those people live?

Until that question is addressed honestly, calling landlords parasites may feel righteous, but it does nothing to solve the crisis it claims to oppose.

Sources and Further Reading

Ministry of Housing, Communities & Local Government (MHCLG), Live Tables on Housing Supply and Social Housing Stock

National Audit Office (2023), Local Authority Housing and Temporary Accommodation

Institute for Fiscal Studies, The Decline of Social Housing in England

Resolution Foundation, Housing Supply, Affordability and the Private Rented Sector

Shelter England, Social Housing Waiting Lists and Temporary Accommodation Statistics

Office for National Statistics (ONS), Housing Costs and Household Expenditure

Centre for Cities, Planning Constraints and Housing Delivery in the UK

Joseph Rowntree Foundation, Housing, Poverty and Inequality

Budget 2025: The Moment the Old Property Game Ended, And Why the Next Era Belongs to the Operators

The Budget has barely cooled, and already the usual storms of commentary are beginning to form, headlines without context, soundbites without analysis, outrage without understanding. Yet buried beneath the noise is something far more profound than a few changes to tax rates or reliefs.

Budget 2025 is not just another fiscal event. It is a declaration of intent. It signals a fundamental repositioning of how the UK treats work, capital, and, most importantly, the people who take risks to build businesses, homes, and prosperity. The changes aren’t simply financial. They’re philosophical. And if you’re a property entrepreneur, this Budget marks a turning point that has been quietly building for years.

2025 Budget

The Budget has barely cooled, and already the usual storms of commentary are beginning to form, headlines without context, soundbites without analysis, outrage without understanding. Yet buried beneath the noise is something far more profound than a few changes to tax rates or reliefs.

Budget 2025 is not just another fiscal event. It is a declaration of intent. It signals a fundamental repositioning of how the UK treats work, capital, and, most importantly, the people who take risks to build businesses, homes, and prosperity. The changes aren’t simply financial. They’re philosophical. And if you’re a property entrepreneur, this Budget marks a turning point that has been quietly building for years.

A New Tax Architecture — and What It Really Means

For decades, the British tax system has been structurally biased toward salaried employment. What Budget 2025 does is complete a shift that’s been telegraphed for some time: the migration from taxing work to taxing wealth, or at least the version of wealth most accessible to ordinary people.

The headline example is the creation of a dedicated, higher-taxed category for property income. For the first time in modern UK history, rental income will sit in its own silo, taxed at levels that exceed comparable bands for earned income. Dividends will rise in 2026, savings income the year after, and council tax will now punish owners of £2m+ homes with a new “high-value” surcharge.

On the surface, the political narrative is familiar: this is about fairness. About ensuring that wealth contributes proportionately. About generating fiscal space after years of stagnation. But fairness is not a slogan. It’s a system. And this particular system raises a rather uncomfortable question. Because the people earning high volumes of rental income or pure UK dividends are rarely the ultra-wealthy.

Serious wealth is global, mobile, structured, and protected. Meanwhile, small landlords, professionals with a handful of assets, and SME business owners… the backbone of Britain’s entrepreneurial class, find themselves caught in a tightening net. It’s not the billionaire with offshore trusts who will feel this. It’s the couple with three rentals who built them slowly over twenty years. It’s the contractor who incorporated for flexibility. It’s the regional investor whose portfolio is their pension.

Budget 2025 doesn’t tax the rich. It taxes the aspirational.

The End of Passive Landlording

The most seismic shift in the Budget is the effective dismantling of the traditional buy-to-let model. The combination of higher property income tax rates, the ordering of reliefs that deprioritise landlords, and the cumulative impact of previous measures (like the erosion of mortgage interest relief) sends a clear message: Passive property investing is no longer welcome as a mainstream path.

The government’s theory is simple: passive rental income is unearned and therefore should be taxed more aggressively. But theory rarely collides neatly with reality. Because when you disincentivise small landlords, the people who step into the vacuum aren’t charities or social housing providers.

They’re institutions. Institutional landlords, build-to-rent conglomerates, REITs, pension funds, these are the players with the balance sheets to absorb tax changes, buy housing at scale, and shape markets. The Budget may end up accelerating a transition the public never voted for: the consolidation of the UK rental market into corporate hands.

The irony is stark. A government attempting to fix the housing crisis may inadvertently create a landscape where individuals have less ownership and less control over housing than ever before.

2025 Budget

The Squeeze on Entrepreneurs

The business owner sits at the intersection of this new tax architecture. Rising dividend tax, frozen thresholds, restricted salary sacrifices, each measure taken alone is survivable. But taken together, they represent the heaviest combined tax load on small business owners in decades. This matters, because property entrepreneurs exist in a unique hybrid space. They create homes and run companies. They generate rental income and operate businesses. They are both investors and employers.

Taxing them more heavily while simultaneously expecting them to regenerate high streets, convert commercial units, revitalise town centres, and deliver housing stock is a strategic contradiction.

You cannot simultaneously demand more from the people willing to take risks while making the act of taking risks less rewarding. Yet that is precisely what the 2025 Budget does.

The Great Contradiction: Build More, Tax More

This contradiction sits at the heart of the Budget.

On one hand, the government has laid out the most ambitious pro-housing agenda in over a decade. Reforming the NPPF, boosting planning capacity, hiring 350 new planners, targeting 1.5 million homes, accelerating infrastructure: these are serious, overdue commitments that speak to a nation in urgent need of new supply.

But supply does not create itself. Homes are not built by committees. They are built by entrepreneurs, people who take on risk, debt, planning uncertainty, operational challenges, and the volatility of markets.

And so we arrive at an unavoidable tension: You cannot tax the people you need to deliver national objectives and expect output to remain the same. If the goal is to build more homes, regenerate more towns, and revitalise more high streets, then you need more, not fewer, property entrepreneurs. You need individuals who are capable of reading markets, designing strategies, adding value, structuring deals, and delivering outcomes. Right now, the Budget helps the planning system but hinders the people who actually utilise it.

2025 Budget

The Winners, the Losers, and the Vacuum in Between

There will always be winners in any fiscal event. Institutional investors will continue to expand. Mixed-use developers will benefit from business rates support. Regeneration specialists will flourish. Operators with legitimate commercial models will do well. Those holding assets in sophisticated corporate structures will find themselves relatively insulated.

But the casual landlord, the owner of two or three rentals, the higher-rate taxpayer with property in personal name, these individuals will struggle to make the numbers work. And while some will leave the sector altogether, others will be absorbed into an increasingly corporatised rental market.

What emerges is a “barbell effect”: large institutions on one side, specialist operators on the other, with ordinary landlords squeezed out of the middle.

The Rise of the Operator — And the Proof That the Unicorn Model Was Always the Future

For years I’ve argued that the era of passive property income is ending. The sector has been moving towards a professionalised, value-add, operationally intensive model for some time. Budget 2025 simply accelerates what was already inevitable. High-yield strategies, mixed-use conversions, HMOs, serviced accommodation, FRI commercial deals, planning-led uplifts — these approaches do not rely on tax favourability to survive. They rely on skill, execution, structure, and operational excellence. They are the domain of the operator, not the landlord.

This is the heart of what I call the Property Unicorn: A model built not on speculative capital growth, but on the intelligent creation of value.