Why You’re Losing £100,000s on Property Deals, And What to Do Instead.

The UK property market is full of smart people doing dumb things with good intentions.

Every week, I meet well-meaning investors, many of them first-time landlords or early-stage buyers, who proudly tell me they’ve secured a couple of shiny new flats off-plan in a so-called “hotspot.” They show me brochures, cite forecasted growth percentages from regional reports, and wait for applause.

But here’s the brutal truth:

Most traditional buy-to-let investors are throwing away hundreds of thousands of pounds over the next decade, all because they’re investing the wrong way.

It’s not because they’re lazy or reckless. It’s because the model they’re following is fundamentally flawed. It’s built on assumptions that no longer hold true in the current market.

Let’s unpack this, and more importantly, let me show you a better way.

The Standard Buy-to-Let Blueprint (And Why It’s Broken)

Let’s say you have £100,000 to invest in property, a typical figure for many first-time investors, family landlords, or people cashing in a pension lump sum.

The advice they’re often given is simple:

“Put down 25% deposits on a couple of new-build flats in a regeneration area. Let them out. Hold for capital growth.”

Sounds solid. Let’s run the numbers.

Take this real listing in the North West — a region heavily marketed for “growth potential”:

Price: £200,000 per unit

Deposit (25%): £50,000

Plus SDLT, legal fees, mortgage setup, furnishing, etc.: ~£16,500

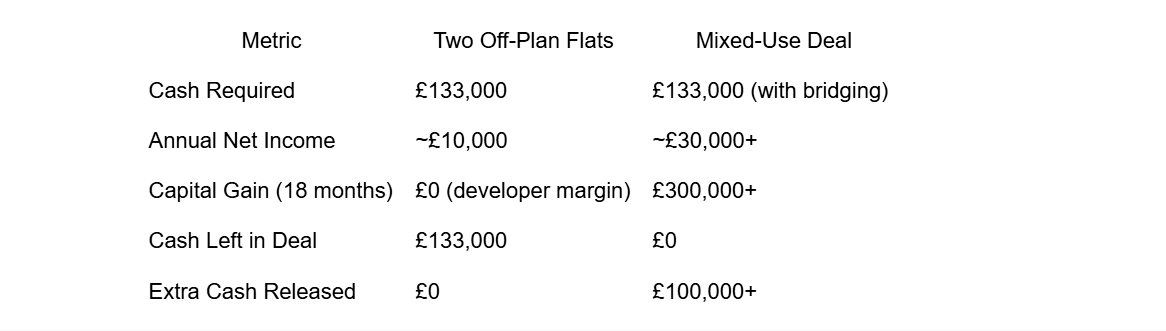

Total cash required for two units: ~£133,000

So far, so typical.

Now, what do these flats return?

Gross Rent per unit: ~£10,000/year

Mortgage interest: ~£5,000/year

Net profit per flat (before tax, voids, and maintenance): ~£5,000

Total net return on capital: £10,000/year or ~7.5% gross / ~2.15% net yield on cash invested

And this is best-case scenario before tax and assuming no repairs or voids.

Here’s the kicker: investors are told that a 28.8% growth forecast over the next 5 years will make this model work.

But this thinking is backwards.

Why?

Because they’ve paid full market (or developer-inflated) price. If the value does rise 30% over 5 years, that simply brings them back to true market value, not ahead of it.

They’re not banking profits. They’re just clawing back the premium they overpaid in the first place.

A Better Model: Create Value, Don’t Wait for It

Let’s take the exact same cash, £133,000 and apply a different model.

In 2023, I purchased a tired mixed-use building for £345,000. It wasn’t flashy. It wasn’t off-plan. But it had something far more valuable:

➡️ Undervalued income potential.

We spent around £75,000 on light cosmetic upgrades. Nothing structural. No planning permission. No new build complications. Just:

White-boxing the retail unit to make it lettable

Re-engineering the tenancy structure for efficiency

Modernising the internals with simple layout tweaks

Within 18 months:

The building was independently valued at £750,000+

It now generates £5,000+ per month in rent

We used open-market bridging finance to buy and refurbish

On refinance, the new valuation allowed us to pull out our original £133,000, plus an additional £100,000 in working capital

That’s £233,000 in the bank, a cashflowing asset, and none of our original money left in the deal.

Let’s compare that to the two off-plan flats.

The Hidden Problem With “Safe” Investments

Off-plan and turnkey buy-to-lets are marketed as “hands-off,” “low-risk,” and “guaranteed growth.”

But let’s be honest, when a developer offers a guaranteed rent, it’s not a gift. It’s priced into the sale. And when you buy something brand new, you’re not buying value, you’re buying someone else’s margin.

Here’s the uncomfortable truth:

You are the exit strategy for someone else’s value-add model.

They bought the land cheap, got planning uplift, built at scale, added margin, and now sell to retail investors who believe they’re securing “growth.”

By contrast, the Unicorn Model I use is about finding assets that are:

Undervalued at purchase

Capable of income or layout re-engineering

Able to refinance based on real, forced uplift, not speculation

This allows you to get your capital back fast, and then reuse it, again and again.

The Real Power of Rinse-and-Repeat

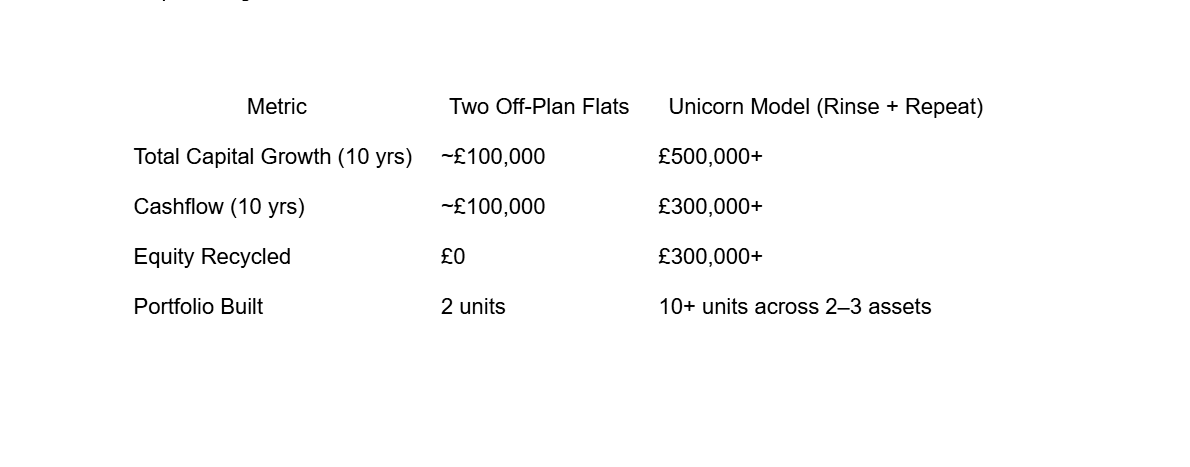

After refinancing that first deal, we used the surplus capital to buy a block of seven flats.

That block now rents for over £100,000 per year. The cash pot that was tied up in two underperforming flats in the mainstream model now controls:

A cashflowing mixed-use asset

A block of 7 residential units

A combined income stream over £130,000/year

Equity growth from two assets

That’s the difference between buying like a landlord and thinking like a developer.

And we did it all with the same original £133,000 that would’ve gone into two off-plan boxes.

Let’s Talk Compounding

The final point most investors miss is this: compounding only works when your capital can move.

When your cash is locked in a deal, even a good one, it’s not compounding. It’s stagnating.

By extracting your capital through refinance, you keep your capital in motion, and that’s when compounding kicks in.

Let’s compare the 10-year outlook of the two models, assuming just 4% annual growth (far below the 28.8% some are sold on):

Final Word: Don’t Buy Property. Engineer It.

Stop buying what’s being sold to you.

Stop waiting for growth to save a poor decision.

Stop assuming that “property always goes up” is a strategy.

What worked for landlords in 2005 does not work in 2025.

The gap between high-street investor and high-performing operator is widening. You either learn how to play like a pro,or you become someone else’s exit.

The good news?

This model isn’t a secret.

It’s not a gimmick.

It’s not reserved for developers in suits with six-figure bank accounts.

It’s systemised, repeatable, and fully explained in my book, Property Unicorn.

📘 Want the full step-by-step playbook?

I’ll send you a free copy of the book. Just hit the link and request it. No charge — just the system we use, backed by real numbers, that works in today’s market.

Stop hoping. Start engineering.

— Rob