Why Property Gurus Are Stuck in 2010 — And How AI Is Changing the Game

In 2010, you could get ahead with hustle alone. You could outwork the competition, knock on doors, and build your portfolio by sheer persistence.

In 2025, that same approach is slow, inefficient, and blind to the biggest edge investors have today: data.

Walk into almost any property seminar in the UK today, and you’ll hear the same script you could have heard in 2010. The same PowerPoint slides. The same “insider tips.” The same pitch for a £15,000 training package that promises to unlock the secrets of financial freedom.

The problem is, those “secrets” are ancient history.

The playbook still looks like this:

View 100 properties.

Post letters to landlords begging them to sell.

Hunt for “tired stock.”

Rely on “gut feel” to know a good deal.

That might have worked in 2010. The market was different, competition was thinner, and if you had the stamina to knock on doors and the patience to drown in spreadsheets, you could scrape an edge.

But in 2025? That model is broken.

The Old Model: Built on Hustle, Not Insight

I started investing around the tail end of that old world. Back then, hustle was everything. If you had the energy to chase deals, view property after property, and sit at the kitchen table with an owner until they signed, you could make money.

The “gurus” of that era built empires on persistence. They sold the idea that property success was about grit: who could send more letters, make more calls, and throw more offers against the wall.

The irony is, they’ve never updated the script. They’re still teaching hustle as the answer, long after the game has changed.

And here’s the truth nobody on those stages will tell you: hustle alone doesn’t win anymore. The investors who rely purely on shoe leather and charm are losing to those who’ve embraced a new edge — data.

The Market Isn’t What It Was

There are three big shifts that broke the old model:

1. Regulation

Buy-to-let in 2010 was the Wild West. Licensing was patchy, HMOs were loosely enforced, and lenders were generous. Fast forward to today, and the regulatory net is tight. Section 24 wiped out tax relief, EPC standards are tightening, and licensing is aggressive. If you’re flying blind on “gut feel,” you’ll end up owning liabilities, not assets.

2. Data Explosion

In 2010, most investors relied on Rightmove, Zoopla, and an Excel spreadsheet. Now, every metric you could imagine is online. You can track rental yields street by street. You can scrape planning applications. You can analyse ownership history. If you aren’t using data, you’re effectively competing with a blindfold on.

3. Competition

Property isn’t fringe anymore. It’s mainstream. Institutions are muscling into markets where private landlords once dominated. Crowdfunded platforms are raising millions. International investors are scouring regional towns. If you think you’ll beat them by licking stamps and sending landlord letters, good luck.

Why Most Gurus Haven’t Moved On

So why do most property trainers keep recycling the 2010 playbook?

Simple: it’s easy to sell.

“Send 500 letters to landlords” sounds achievable. “View 100 houses” feels like tangible work. People like to believe success comes from doing more of what’s familiar.

But here’s the problem: familiarity doesn’t equal effectiveness. While students are pounding pavements, institutional investors are running predictive models that identify undervalued stock before it even hits the open market.

That’s the real playing field. And if you’re paying five figures for a training course that ignores it, you’re paying for nostalgia, not strategy.

The New Reality: Systemised, Data-Led Investing

In my business, I’ve built a system I call RobBot. It’s an AI-driven toolkit that sits at the heart of every decision I make.

Here’s what it does:

Appraises 50+ deals in seconds using my exact criteria for yield, margin, and value-add potential.

Sorts opportunities by profitability and vendor motivation, so I only spend time on the best ones.

Generates negotiation scripts tailored to seller behaviour patterns. If a vendor is risk-averse, it frames the offer one way; if they’re cash-hungry, another.

Writes offers, contracts, and operational documents without me staring at Word templates for hours.

Tracks live performance across lettings, refurbishments, and cashflow, flagging issues before they become disasters.

That’s not theory. That’s running in my business today.

And while the old-school gurus are still telling people to “trust their gut,” I’m making decisions backed by thousands of data points — in seconds.

Why AI Doesn’t Replace Strategy — It Amplifies It

The predictable pushback is: “But AI doesn’t understand property. You still need human experience.”

Correct.

AI doesn’t replace the need for strategy. It doesn’t replace the judgement to know which market cycle you’re in, or the creativity to structure a win-win deal. What it does is supercharge your ability to apply that strategy at scale.

Think about it this way:

Without AI, 90% of my time used to be wasted chasing dead ends.

With AI, 90% of my time is spent executing the top opportunities.

It’s not about working harder. It’s about eliminating everything that doesn’t move the needle.

The Gurus Are Playing Checkers. AI Investors Are Playing Chess.

Here’s the biggest shift AI creates: the playing field isn’t level anymore.

The investors clinging to the 2010 playbook are competing in a slow, linear way. View. Offer. Wait. Repeat.

Meanwhile, data-led investors are compounding speed and accuracy. When I analyse 50 deals in the time it takes them to look at one, the outcome isn’t even close.

This isn’t theory. It’s happening now.

Where AI Is Already Transforming Property

If you think this is “sci-fi,” you’re already behind. AI is being applied in property across the board:

Valuation models that beat Zoopla estimates.

Predictive rent analysis that forecasts demand shifts street by street.

Automated compliance tracking that flags EPC or licensing risks before they cost you.

Conversational AI agents handling tenant queries.

Automated finance structuring that identifies the most efficient mortgage and debt solutions.

And that’s just 2025. In five years, investors who don’t integrate AI will be as outdated as those still using fax machines.

The Human Edge Still Matters

Here’s the nuance: AI doesn’t kill the need for humans. It kills the need for human inefficiency.

AI won’t walk a property and notice rising damp. AI won’t build rapport with a vendor who’s going through divorce. AI won’t spot the political dynamics of a council planning committee.

That’s where the investor’s edge lives now: not in trawling spreadsheets, but in applying human judgement where it counts most.

The winners of the next decade will be those who combine human insight with machine efficiency. Not either/or. Both.

Why Most Investors Won’t Make the Leap

If AI is so powerful, why isn’t every investor using it?

Because change is uncomfortable.

It’s easier to believe success is about knocking on more doors than learning a new system. It’s easier to keep paying gurus who tell you the old hustle still works than to admit you need to upgrade your skills.

And let’s be blunt: a lot of investors like the story of being busy. It makes them feel in control, even if they’re not actually making money.

But stories don’t build portfolios. Numbers do.

The Players Are Changing

This is why the property game is being reshuffled. The next wave of successful investors won’t be those who grind hardest. It’ll be those who systemise smartest.

The amateur landlord with a spreadsheet is outgunned.

The seminar junkie chasing 2010 strategies is outpaced.

The data-led investor with an AI stack is scaling faster, safer, and smarter.

That’s the shift.

The Summit: Where This Goes Next

At the Property Unicorn Summit this September, I’ll be pulling back the curtain on how this works in real time. Live examples. Real data. Operational systems investors can implement immediately.

Because here’s the choice every investor faces:

Stick with the 2010 playbook, grinding harder for diminishing results.

Or embrace the tools that define 2025, and position yourself for the next decade of growth.

One option feels comfortable. The other option builds wealth.

Final Thought

The gurus teaching today aren’t wrong because they were never right. They’re wrong because they’ve frozen in time.

They’re still selling the story that hustle equals success. But in 2025, hustle without data is noise.

The investors who thrive in the next decade won’t be those who knock on the most doors. They’ll be the ones who combine timeless strategy with AI systems that give them exponential leverage.

That’s not the future. That’s now.

Property Unicorn Summit this September, I’ll be showing exactly how to build an AI-powered property business. Live examples. Real numbers. Systems you can implement immediately.

Bet Everything on a property Crash. It Worked.

Bet Everything on a property Crash. It Worked.

In 2022, interest rates started rising faster than we’d seen in over a decade. Panic set in. The market wobbled. And I made a move most people would call mad:

I sold my home.

I took 15 years of experience in property and went all in—on a crash.

Why I Sold at the Peak

I could see what was coming:

Cheap money was disappearing

Yields were thinning

The commercial market was headed for a reset

So I sold my house near the peak of the market, went into cash, and moved into a rental.

It sounds backwards, right? But here’s the trick most people miss:

Using the law of diminishing rental returns, we could rent a house far nicer than we could buy. For less money, less commitment, and more flexibility.

My partner Helen did the same. Together, we freed up about £500,000 in liquidity.

Strategy in Motion: Go Where the Crash Hits First

We set up a 50/50 SPV (Special Purpose Vehicle) and went deal hunting.

Our first move?

We bought a commercial block for £345,000 in early 2023—cash.

This was right after Liz Truss’s infamous mini-budget, which tanked market confidence and made sellers more negotiable.

We put around £70,000 into cosmetic works—whiteboxed it, modernised the layout, let the commercial space, and turned three of the four flats into Airbnbs (with a tenant still in the fourth).

The Results? Not Hype—Hard Numbers

Just had it revalued at £795,000

That’s £350,000+ in equity created

Rental income: £60,000+ a year (before finance)

This wasn’t theory—it was strategy in motion.

Deal #2: Leveraging Up with Precision

With the remaining funds—and a portfolio facility secured on property #1—we bought our second site:

A block of 7 tenanted flats for £825,000.

As tenants moved out, we converted each one into boutique Airbnb units.

As of now, we’ve flipped 4 out of 7. The current valuation?

Over £1 million—and tracking toward £1.2 million once the last 3 are done.

📅 This July alone: Airbnb bookings hit £16,000 gross.

That’s enough to:

Pay out tax-free director’s loans to cover our rent

Leave the rest in the company to compound for the next deal

So... Madness or Strategy?

In under two years, without external investors, we’ve:

✅ Built a portfolio generating enough net cashflow to cover all our personal living costs

✅ Created over £500,000 in equity

✅ Maintained full control by using only the equity in our homes

Meanwhile, many higher-end homeowners are watching their valuations slide.

We moved when others froze. We bet on a crash—and we had a plan to make it work.

Your Move

Was it risky? Yes.

Was it reckless? No.

It was informed, timed, and executed with intent.

The question is—would you have done it?

👇 Drop your take in the comments.

Want to see how we’re building in this market, without fluff or fairy tales?

Click Here for you free copy of Property Unicorns

50% Property Price Crash Warning? Let’s Talk Facts

Scroll through social media or click on a tabloid headline, and you’ll hear it:

“The mother of all property crashes is coming.”

Some even predict drops of 30% to 50%.

Cue panic. Cue clickbait. Cue doomscrolling.

But let’s have a real conversation about property cycles, because context matters more than panic.

I scroll past doom‑scrolling headlines and guff about a “mother of all crashes.” Supposedly, we’re staring down the barrel of a 30 % to 50 % collapse. That’s terrifying. But how much of that is fear and how much is fact?

I’m digging for truth: not hype. Here’s the breakdown, pulled from data, not panic, and I’ll punch holes in the absurdity of clickbait.

Are Property Crashes Really Getting Worse?

Quoted lines like “the highs are getting higher, and the lows are getting lower” sound slick. But digging into the numbers, volatility hasn’t grown, it’s softened.

Academic studies show that UK housing volatility is stabilising. A paper using ARCH/GARCH models finds three different volatility regimes—yet transitions between them are rare, meaning the market isn’t swinging more wildly now than before GOV.UK Assets+2MoneyWeek+2ResearchGate+1.

Real terms fluctuate—sure: in 2009, real house prices plunged by 16 % across the UK and 29 % in Northern Ireland Economics Help+4pearsonblog.campaignserver.co.uk+4Oxford Academic+4. But on average, real house prices grew at just +3.2 % above inflation per year between 1970 and 2019 LSE Personal Pages+15pearsonblog.campaignserver.co.uk+15SpringerLink+15. That’s resolute, slow‑and‑steady growth, not volatile freefall.

Since 2008, we’ve been living in a low‑growth, low‑volatility era. Household affordability hasn’t budged—post‑2008, real wage growth shrank to near zero, and property growth slowed accordingly Economics Help.

Why Today Feels More Volatile Than It Is

Michael Bay‑style headlines are sensational: £14,000 wiped off house values! But that often turns out to be just 3 %–5 % of value lost. It’s dramatic, but not cataclysmic.

Meanwhile, in June 2025, UK average house prices rose 3.7 % year‑on‑year, to an average of £269,000. Monthly growth was 1.4 % Office for Budget Responsibility+3GOV.UK+3The Guardian+3. Regional differences are telling: North‑East house prices jumped 7.8 % annual, London barely ticked up 0.8 % GOV.UK.

That north‑south divergence isn’t new, but it’s more pronounced: root is affordability and banking on “southern premium” no longer holds water The TimesFinancial Times.

So yes, people feel jittery—but the data says this is performance‐art. Not apocalypse.

The New Regime: Dampened Boom, Prolonged Plateau

What transformed the market?

Stricter lending post-2008 means bigger deposits and smaller leverage Financial TimesThe Times

Help to Buy schemes injected demand—but didn’t fix supply, especially in constrained areas like London The Times+5en.wikipedia.org+5pearsonblog.campaignserver.co.uk+5

Regulation and risk controls, including stress testing, have smoothed cycles.

The result: national house prices inch up rather than surge. The OBR forecasts growth of just 2.8 % in 2025, and an average of 2.5 % through 2029, bringing UK average price to around £295,000 by end of decade Office for Budget Responsibility.

This isn’t a crash lockdown….it’s a slow cruise control. More headline-friendly than catastrophic.

The Real Danger: Overleverage, Not Volatility

Sure, cycles still exist. Crashes still happen. But the bigger risk now is buyers overextended on margin, not dramatic 50 % price swings.

If you bought at the peak, stretched your deposit, or relied on future inflation to bail you out, you’re the one exposed, not the market.

This isn’t about wild cycles anymore, it’s about being prudent in a low-growth environment.

So … Is a 50 % Crash Coming?

Let’s be blunt: Noble prize-level data doesn’t back that claim.

We may expect localized corrections, regional softness, maybe a recession-prompted slowdown. But a full-blown 50 % crash across the UK? Not seeing the evidence.

What’s real is a policy-driven, technical market, not a rollercoaster. Lending standards, regulation, and demographic shifts have fundamentally changed the system.

A Better Strategy Moves Beyond Panic

If you’re in property, don’t chase the booms or fear the busts. You want a method that works in any cycle stage.

That’s where The Unicorn Concept comes in: commercial valuation models, unused housing stock, resilient income….not hype.

Summary: Flattened Cycles, Not Collapsed Markets

Insight Reality

Property crashes are deeper now No. volatility has softened.

Dramatic headlines reflect systemic risk No. often just imbalanced optics.

Real danger is leverage risk Yes, being overexposed is why people suffer.

50 % crash is likely? No, tiny chance, not across the board.

Market’s future Technical, regional, resilient, if played smart.

I’m not saying everything’s peachy. But crying wolf about apocalypse won’t help anyone. If you’re investing or advising, you’re better off seeing the signal, not the noise.

Property Unicorns (that inevitably-shameless plug) walks you through strategies that survive cycles, ignore doom, and actually build value.

👉 Grab your free copy here of my book and learn how smart investors are still creating income, equity, and scale, even in a “crisis.”

46 Applications. One Flat. This Is the Crisis.

Last week, I listed a flat in Chester. Within 48 hours, it had 46 enquiries.

Forty-six. For one flat.

This wasn’t a luxury penthouse or underpriced deal, it was a standard two-bed that had been rented to a housing association for the past 10 years. As the lease ended, I decided to bring it back into the private rental market.

I stuck it on OpenRent, expecting a decent response.

What I got was a flood of messages, young professionals, NHS workers, teachers, all scrambling for a place to live.

This isn’t just a hot market.

This is a housing crisis.

I listed a two‑bed flat in Chester—nothing fancy, rented by a housing association for a decade. Within 48 hours, I had 46 enquiries. Yes, forty‑six. That many people chasing the same slice of shelter. I didn’t expect this tsunami—not because the flat was a stealth gem, but because the market is desperate. This isn’t just hot: it’s a full‑on housing emergency masquerading as consumer demand.

Let me get blunt: buy‑to‑let isn’t dead. It’s fundamentally broken.

Supply Collapsed While Demand Exploded

Let’s get the numbers out of the way before any feel‑good illusion kicks in. Beginning with competition: as of March 2025, there were about 12 renters chasing every available home The Times+8fraser.uk.com+8The Times+8. That’s twice the pressure from before the pandemic. So when my flat attracted 46 applications, I wasn’t witnessing a fluke; I was seeing the systemic breakdown writ small.

Rental inflation since September 2022? Every single month clocked 5% or more year‑on‑year rent growth, setting a pace not seen since records began in 2005 Resolution Foundation.

And the cost isn’t trivial. In June 2025, private renters faced 4.5% annual inflation, outpacing the national average of 3.9% Hometrack+15Financial Times+15Zoopla+15.

Over three years (2022–2025), average UK rents jumped 21% (about £221), while average mortgage payments only rose £218 MoneyWeek. Renters are shouldering more, borrowing less.

Even rent‑to‑income ratios are ugly. In England, renters fork over around 36% of their gross income, and in London it’s over 40% Landlord Knowledge.

So yes, people need housing. Desperately. The plays for supply can’t keep pace.

Why Buy-to-Let Isn’t Dead—or Rather, Why It Has to Be Reinvented

Let’s dismantle the usual excuses:

‑ Mortgage rates doubled in two years. Rate‑hiking central banks and refinancing nightmares obliterate margins.

‑ Tax changes? Landlords got squeezed from all sides: the stripping of mortgage interest relief, new tax burdens. Now NI on rental income is on the table, which could push about 40% of landlords out, according to analysts Felix Accountants+2fraser.uk.com+2The Times+1.

‑ Regulations pile up with zero win for tenants or investors. Energy efficiency demands, deposit caps, safety standards, licensing—tons of red tape. The Renters’ Rights Bill, currently circling Parliament, aims to ban fixed‑term assured tenancies, impose new decent‑home standards, force landlord databases, and squeeze bids—yet does nothing to fix stock scarcity Wikipedia.

The result: landlords are bailing. RICS reports the steepest drop in new rental listings since the first COVID lockdown The Guardian. Another survey shows landlord instructions dropped a net ‑21% in June 2025, even while tenant demand barely fell (‑2%) The Times+11Landlord Knowledge+11The Times+11.

Supply is fragile because buy‑to‑let isn’t rewarding enough anymore.

The Demand Is Still Boiling Over

When I list a normal two‑bed, I don’t get 5 applications. I get 46.

That’s not scarcity…it’s starvation!

Rental stock remains about 20% below pre‑pandemic levels, despite a 17% increase in supply compared to a year ago MoneyWeekWikipediaThe TimesZoopla. So yes, we’re climbing back up, but from rock bottom.

Every region varies, but the pressure is nationwide. In Chester, rents grew 8.2%; Wigan, 8.8% Zoopla. In London, average rent now hits £2,712 a month, while the rest of the UK sits at £1,365 The Guardian.

This isn’t a blip. It’s systemic. Renters can’t find listings; landlords can’t make it work; politicians keep announcing reforms that don’t fix the basic mismatch.

Enter: Urban Goldmines: Repurposing What Already Exists

Let’s talk models. Building from scratch is expensive, slow, planning‑paperwork hell. Meanwhile, homelessness and precarious housing proliferate.

We look up, not out. Empty space above shops, defunct B&Bs, redundant commercial units, they’re everywhere. Everyone ignores them.

We don’t. We convert, reconfigure, and attach residential use. We value them commercially to make the numbers work, then transform them into clean, decent, rentable homes. It’s not buy‑to‑let as you were told, it’s property entrepreneurship.

We’re building supply, solving problems, creating value that sticks.

Policy Is Playing Catch-Up…or Passing You By?

The brave new world’s trying to regulate everything. The Renters’ Rights Bill wants to dampen bidding wars and improve standards, but nothing in there actually creates more housing fraser.uk.com.

Meanwhile, councils are desperate. In England, 37 councils shelled out £31 million on one‑off payments to private landlords housing homeless families….sometimes more than £10,000 each. Incentives surged 54% since 2018 in London alone The Guardian.

Build‑to‑Rent, the big institutional bet? Doesn’t cool prices. In areas with tons of BTR units: Brent, Ealing, Manchester, rents rose faster Financial Times.

Savills warns rents will climb nearly 20% over five years, driven by supply gap and landlord retreat The Times.

So while policy debates swirl about taxes and rights, nobody’s actually building the homes people need. Municipal budgets explode on landlords to plug holes. Build-to-Rent swells supply on paper but pushes up prices in reality.

This Is the Future: Creative, Real, Entrepreneurial

Urban Goldmines are not sexy. They’re practical. They turn waste into homes. That’s real impact.

I’m not flipping for yield—those yields don’t exist anymore. I’m building something long-term: wealth, yes, but also resilience, better housing, smarter city fabric.

That’s what Property Unicorns—my book—lays out. This isn’t my shaky speculative side hustle. This is the future of housing investment, and of housing access.

Wrap

Let’s stop kidding ourselves. The rental system is broken, not dead. Demand is feral. Supply is thinning. Policy is parading while real solutions lurk in overlooked buildings.

Urban Goldmines aren’t the cure, but they’re the lifeline too few are grabbing. If you want to stop complaining and start building, that’s where the real work, and the real reward, is.

Book pitch, final note: Property Unicorns shows you how to do it. Not flipping, not sham yield-seeking. Municipal-smashing, city-fixing, housing-making. Want a copy? Say “Unicorn” or hit the link.

[Order your free copy of my book here → LINK]

How I Bagged £145K in Equity Overnight

Ever pulled £145,000 of equity out of thin air?

I did. And no, it’s not clickbait or fluff, it’s called yield compression. Most investors don’t talk about it because they don’t understand it. But if you want to make serious gains without swinging a hammer, listen up.

Let me break it down in plain English.

Without a Single Renovation.

Ever pulled £145,000 of equity out of thin air?

I did. And no, it’s not clickbait or fluff, it’s called yield compression. Most investors don’t talk about it because they don’t understand it. But if you want to make serious gains without swinging a hammer, listen up.

Let me break it down in plain English.

The Power Equation

In commercial property, value isn’t based on emotional buyers or Zoopla estimates. It’s simple maths:

Property Value = Net Rent ÷ Yield

So when yields go down, values go up. That’s the game.

Real Deal Numbers, No Theory

In 2023, I looked at a commercial block pulling in £85,000 annual rent. The market was pricing it at a 9.5% yield, which pegged its value at around:

£85,000 ÷ 9.5% = £895,000

But something didn’t smell right.

We dug in. The landlord was covering some costs behind the scenes, so the real net income was even lower. That yield was worse than advertised.

I didn’t want the headache. I wanted a clean 10% return on real numbers. So I negotiated, hard, and locked in a deal for:

£825,000

Already a win, right? Not even close.

Then the Market Shifted…

Before I even got the keys, the valuers in Chester updated their assumptions. The area was now valuing assets like this at 8.5% yields.

Same rent. Lower yield. Higher value.

£85,000 ÷ 8.5% = £1,000,000

Let’s be conservative and call it £970,000.

I hadn’t touched the place. No refurb. No upgrades. Just £145,000 of equity created, overnight.

That’s Not All — Stamp Duty Trick

Most buyers throw money at stamp duty like it’s non-negotiable. Not me.

I used Multiple Dwellings Relief (MDR), which cut my stamp duty bill from £70K down to £20K. That’s a £50,000 saving, enough to buy a Tesla before I even got the keys.

Phase 2 — Pump the Income

Once we had the asset under control, it was time to optimise.

Every time a tenant moves out, we refurb the unit and flip it to short-term lets, mostly Airbnb. These net about 50% more rent per unit compared to long-term tenants.

Our projected net income in a few years? £120,000 annually.

At an 8.5% yield, that puts the asset’s value around:

£120,000 ÷ 8.5% = £1.41 million

Not bad for a property bought under market and lightly improved.

Final Word — This Is the Game

This isn’t a one-off. It’s the model:

Buy fat. Revalue skinny. Laugh all the way to the bank.

That’s yield compression in action.

Stop focusing only on the bricks. Start learning how commercial valuation works. It’s where the real money is made—without touching a paintbrush.

Want to Learn This Game?

I break this down step-by-step in my free video training and inside my book. No fluff, no guruspeak—just real numbers and proven strategies.

👉 [Grab my free book or watch the training here]

How I Turned £50K into £1M Without Building a Thing:

Let me make a bold claim, but back it up properly: you can turn £50,000 into £1 million in profit from a single property, no building extensions, no planning permission headaches, and no pipe dreams. Just well-applied logic, a deep understanding of property mechanics, and a strategy that challenges the mainstream model.

This isn’t one of those hypey “buy ten houses with none of your own money” gimmicks that fill your feed. And no, I’m not about to sell you a dream of infinite passive income on a beach in Bali. This is about what actually works in today’s market if you think differently.

I call it Unicorn Momentum, and it’s how I outpace most developers, landlords, and so-called experts, with far less risk and a lot more control.

And Why the Gurus Have It All Wrong.

Let me make a bold claim, but back it up properly: you can turn £50,000 into £1 million in profit from a single property, no building extensions, no planning permission headaches, and no pipe dreams. Just well-applied logic, a deep understanding of property mechanics, and a strategy that challenges the mainstream model.

This isn’t one of those hypey “buy ten houses with none of your own money” gimmicks that fill your feed. And no, I’m not about to sell you a dream of infinite passive income on a beach in Bali. This is about what actually works in today’s market if you think differently.

I call it Unicorn Momentum, and it’s how I outpace most developers, landlords, and so-called experts, with far less risk and a lot more control.

Step One: The Accidental Goldmine

Back in 2017, I bought a derelict building for £186,000. It was the kind of property even pigeons wouldn’t move into willingly. But underneath the grime was a rare opportunity that most investors would have missed because they’re trained to look for shiny kitchens instead of hidden value.

I split the ground floor into two separate retail units, no extensions, no major construction, just a clever reconfiguration. Those units sold for double what I’d paid for the entire building. That one decision turned a rundown shell into a cash-rich asset almost overnight.

Now, here’s the first critical point: you don’t need to develop to create value. You need to extract value that already exists but is hidden from lazy eyes.

This is the first layer of what I call Unicorn Thinking: spotting what the mainstream misses because they’re too busy chasing cookie-cutter buy-to-lets.

Step Two: Turning Bricks into a Bank

With the capital from that deal, I went upstairs, literally and strategically.

We converted the first floor into 13 one-bed flats. Yes, we needed planning permission for that bit, but here's the difference: I already had the funds created from the asset itself, I wasn’t reaching into my own pocket or scrambling for angel investors.

Once the flats were done, we leased them to the council. That deal now generates just under £80,000 per year in hands-off income.

But the real genius isn’t in the rent, it’s in the equity.

Every improvement, every bit of uplift, was locked inside the building like gold bars behind the walls. And just like a bank vault, that equity can be borrowed against. This is what the banks do. It’s what the institutions do. But individual investors? They’re still buying one house at a time and wondering why they’re not getting ahead.

That’s the flaw in the traditional model. It’s slow, reliant on market appreciation, and increasingly vulnerable to rate rises and regulatory changes.

Step Three: Unicorn Momentum in Action

Fast forward 12 months and we found another opportunity, this time in Chester. A mixed-use building that had been sitting on the market overpriced and overlooked. We used my “Offer Ladder” system to negotiate almost £200,000 off the asking price.

Because I’d already created serious equity in the first property, I didn’t need to scrape together new funds. I leveraged the asset I already had, again, no new borrowing from scratch, just smart recycling of capital. I only needed £50,000 in actual cash to secure the deal.

The building was already kitted out, furnished rooms, a functional layout, and we just refreshed the kitchen. That’s it. That’s the full list of “refurbishment”.

It now rents for nearly £10,000 a month.

Why It Works: Compound Value, Not Volume

This is where the gurus fall apart.

They tell you to buy more. More houses, more mortgages, more risk. But more is rarely better — especially when you're stacking average assets.

I do the opposite. I buy less, but I buy differently.

Each of these deals is engineered to create momentum — what I call Unicorn Momentum. That’s the force multiplier.

Because when you unlock equity without selling, and then redeploy it into the next undervalued, high-cashflow asset, the gains begin to compound — not just financially, but strategically. Each move gives you more leverage, more certainty, and more control.

If I let that £50,000 sit in a fund or used it for a vanilla buy-to-let, I’d be lucky to see 5–6% per year. Instead, we’ve mapped out a ten-year trajectory from that single outlay that’s heading toward £1 million in profit. That’s not theoretical. It’s already in motion.

Why the System Doesn’t Want You Thinking This Way

Let’s be blunt.

The government wants you small. The system wants you predictable. The financial institutions want you to buy at retail price and sit still while they skim your earnings via inflation and interest.

And the property “gurus”? Most of them are just parroting 2010 strategies that haven’t evolved with the market.

You have to go against the current to build real, enduring wealth in property today. That means:

Buying undervalued assets that others don’t understand.

Creating non-construction-based uplift.

Leveraging existing equity, not your personal savings.

And refusing to follow the outdated playbook of stacking low-yield lets and praying for capital growth.

That’s what I teach. That’s what I do. And that’s what works.

If you’re serious about doing things differently, not just louder, but smarter, start thinking in terms of Unicorn Properties, and start building momentum, not just a portfolio.

Because real wealth isn’t about owning more bricks. It’s about owning the right ones — and knowing how to unlock the gold hidden inside.

The £100K Mistake:

Every so often, someone wanders into the property space with sweeping statements like, “If you need bank debt, you shouldn’t be investing.”

Often, it’s a financial advisor. Sometimes, it’s someone with a trauma story from 2008. In this particular case, it was a sleep therapist named Alan, who apparently moonlights as an economist.

His view? If you don’t have the full cash to buy the property outright, you shouldn’t be playing the game.

That sounds safe. Conservative. Responsible, even. But when you break it down — not emotionally, but mathematically — you realise just how deeply flawed that advice is.

Why Buying Property in Cash Is Financially Illiterate.

Every so often, someone wanders into the property space with sweeping statements like, “If you need bank debt, you shouldn’t be investing.”

Often, it’s a financial advisor. Sometimes, it’s someone with a trauma story from 2008. In this particular case, it was a sleep therapist named Alan, who apparently moonlights as an economist.

His view? If you don’t have the full cash to buy the property outright, you shouldn’t be playing the game.

That sounds safe. Conservative. Responsible, even. But when you break it down — not emotionally, but mathematically — you realise just how deeply flawed that advice is.

Let me show you.

The Cash Buyer Illusion

Let’s say you have £100,000 to invest in property. You decide to take Alan’s advice and purchase a single property in cash for the full amount.

It rents for £10,000 per year, giving you a neat 10% yield.

No mortgage, no stress, no leverage. Just clean, slow growth.

Ten years pass. The property doubles in value, fairly reasonable if you’re in the right location and can ride the average UK growth curve. Your £100k asset is now worth £200k. You’ve also collected £100k in rent (ignoring inflation and expenses for simplicity).

Total gain: £200,000.

You’ve effectively doubled your money over a decade. That sounds fine… until you realise what you've left on the table.

The Leverage Advantage

Now let’s look at what happens if you take the same £100k and apply strategic leverage.

Instead of buying one property outright, you split the capital into four £25k deposits and secure 75% mortgages on each. Now you own four properties, each worth £100k, controlling a £400k portfolio with just your £100k invested.

Each unit still rents for £10,000 per year — but this time, you’re paying £5,000 in mortgage interest per property. That gives you £5,000 net cashflow per unit, or £20,000 per year total.

Already, your cashflow return is 20%, double that of the debt-free model. But we’re not done.

The Long-Term Growth Picture

Fast forward ten years. Each £100k property has doubled to £200k.

The unleveraged investor now owns one property worth £200k.

The leveraged investor owns four properties worth £800k in total.

Let’s break down the equity picture:

You still owe £75k per property, or £300k in total.

But the market value is now £800k.

That means you’ve grown your equity position from £100k to £500k a £400,000 gain. That’s four times the capital growth of the cash-only investor.

And all of this assumes you never re-leverage, never refinance, never reinvest rental profits, just hold and wait.

Inflation: The Unseen Ally

Here’s what Alan and the cash-is-king crowd don’t understand:

Inflation punishes cash and rewards debt.

Your £300,000 mortgage doesn’t grow with inflation. But rents and property values do. Over time, your debt gets smaller in real terms, while your income and asset values rise.

In a high-inflation environment — like we’ve seen across 2022–2024 — that difference becomes even more pronounced. You're essentially paying off fixed debt with inflated pounds, while enjoying rental increases that track real-world costs.

This is how banks, institutions, and seasoned investors stay ahead.

It’s how wealth is transferred, not by avoiding debt, but by understanding how to use it intelligently.

The Cost of Playing Safe

Let’s recap the two scenarios over ten years:

Strategy Rent Collected Capital Gain Total Return

Cash Buyer £100,000 £100,000 £200,000

Leveraged £200,000 £400,000 £600,000

Same starting capital. Same properties. Same market.

£400,000 difference in outcome, purely from using leverage.

So let’s be clear: buying in cash is not “safe.”

It’s lazy capital allocation. It’s financial underperformance masked as caution.

It’s the kind of advice that might help you sleep at night… but it’ll cost you dearly in the morning.

What the Gurus and the Government Won’t Say

There’s a broader conversation here.

The system wants you to fear debt. They don’t teach strategic leverage in schools, and they certainly don’t encourage it in mainstream financial planning.

Why?

Because the system isn’t designed to produce investors. It’s designed to produce savers, predictable, risk-averse, inflation-eroded savers who will be sold financial products their entire life.

Debt, when used correctly, isn’t a burden. It’s the engine that drives real asset accumulation.

The problem isn’t leverage. It’s ignorance.

Final Thought: Choose the Right Game

This isn’t just about numbers. It’s about choosing a different financial model, one where you use bank money to control appreciating assets, grow cashflow, and build wealth that isn’t eroded by inflation or taxed by inaction.

You don’t need to be reckless to use leverage.

You just need to be educated, precise, and strategic.

That’s the world we operate in.

That’s the playbook I follow.

And it’s why (while Alan the sleep therapist is waiting for his pension) we’re building real wealth from real assets.

If you’re ready to stop playing small, and start using capital the way professionals do, I’ve got the frameworks and case studies to help you do it properly.

— Rob

The 5 Families of Property Finance:

If you want to scale a property portfolio in today’s market, you need to stop thinking like a borrower and start thinking like a capital allocator.

Most investors rely on one type of funding — usually a high street mortgage — and hope that if they wait long enough or buy enough units, they’ll reach financial freedom.

But in 2025, with higher interest rates, tighter lending criteria, and increasing scrutiny on landlords, that “one-lane” model is outdated. If you want to scale without hitting a wall, you need to understand — and use — the five core families of property funding.

These aren’t tricks. They’re the strategic foundations of how professionals structure and fund their portfolios. Learn them, and you’ll never be stuck waiting on a lender or capital partner again.

If you want to scale a property portfolio in 2025, you can’t think like a borrower anymore. You need to think like a capital allocator.

Most landlords never get that far. They learn one tool — usually a high street buy-to-let mortgage — and then bash it against every problem they face. Eventually, they hit the inevitable wall: stricter lending criteria, affordability stress tests, or a bank that simply says “computer says no.”

That’s when the frustration kicks in. They think they’ve “run out of money” or “run out of borrowing capacity.” The truth? They’ve only run out of imagination.

Professional investors don’t rely on one tool. They build with a full arsenal. And when you zoom out, every creative structure, every “hack” you’ve ever heard about in property, falls into one of five core families of finance.

Learn them properly and you’ll never again be stuck waiting for a lender’s permission slip.

Why the Old One-Lane Model Is Broken

In 2010, you could scale a portfolio with little more than persistence and a clean credit file. Rates were cheap, underwriting was softer, and the game rewarded volume. If you just kept buying, eventually you’d get rich.

That world is gone.

Interest rates are higher. Cheap debt isn’t a given anymore. Every percentage point in the Bank of England base rate changes affordability.

Stress tests are tighter. Many lenders now require rent to cover 145–170% of mortgage payments at notional interest rates of 5–7%. That rules out deals that used to slide through.

Scrutiny is heavier. Landlords are treated like businesses now, not hobbyists. Your track record, tax structure, and compliance all affect whether you get a “yes.”

If you only know how to work the high street, you’re boxed in. To scale, you need flexibility. That’s where the five families come in.

Family 1: Traditional Debt

This is the foundation. Mortgages and bridging loans are still the cheapest capital in the market. If your deal ticks the boxes, this should always be your first port of call.

Loan-to-value (LTV): Typically 60–80%.

Rates: Lower than any other funding source (because banks have the lowest cost of capital).

When to use: Standard properties, strong rental cover, clean borrower profile.

Example: You buy a £200K single-let in Manchester. Deposit £50K, mortgage £150K at 5.5%. Rent of £1,000/month covers the loan with margin. Traditional debt works beautifully here.

The professional edge: Use traditional debt whenever it’s available — but don’t build a strategy that depends solely on it. Because eventually, you’ll get capped by income multiples, portfolio limits, or valuation constraints. That’s when amateurs stall and professionals pivot.

Family 2: Joint Venture (JV) Equity

JVs are the power of alignment. You bring the deal and the execution. Your partner brings the capital. You share the profits — often 50/50.

Use it when: You’ve got strong deal flow but lack liquidity.

Why it works: Removes deposit constraints, allows you to operate faster and at bigger scale.

The trade-off: You split the upside.

Example: You find a block conversion requiring £500K. You’ve got the deal and the contractor team, but not the capital. A JV partner puts in the money. You manage the project. At sale, profits are split evenly.

The professional edge: JVs are high-trust capital. They only work if expectations are clear from day one: how profits are split, how risks are shared, and how decisions are made. The worst JV isn’t when you lose money — it’s when you fall out.

Family 3: Private Notes

Private notes are direct lending arrangements with individuals. They lend you money at fixed returns (8–12% is common) secured against the property or project.

Use it when: You need speed or flexibility.

Why it works: No equity split, less bureaucracy than banks, and you keep the upside.

The trade-off: Higher cost of capital.

Example: A motivated seller wants to complete in 28 days. A bank can’t move that fast. You borrow £100K from a private investor at 10% interest for six months, secured against the property. The deal completes. Later, you refinance with a bank and repay the note.

The professional edge: Private notes are the grease that lets you move when banks stall. Professionals cultivate a network of private lenders precisely so they can strike fast.

Family 4: Asset-Backed Credit Lines

This is where your existing portfolio becomes your liquidity engine. Instead of letting equity sit idle, you unlock it.

Use it when: You’ve built equity in properties and want to recycle it into new deals.

Why it works: It’s revolving. Draw down in days, repay, reuse.

The trade-off: Interest rates can be higher than term loans, and lenders cap against conservative valuations.

Example: You own 10 properties with £1m equity. Instead of refinancing each, you arrange a £500K credit line secured against the portfolio. Now you can fund multiple acquisitions on your own timeline without new mortgage applications.

The professional edge: Asset-backed facilities are how big players scale. They don’t wait six months for every refinance. They keep a war chest.

Family 5: Vendor Finance

This is the most overlooked — and one of the most powerful. Vendor finance means the seller helps fund the purchase.

Use it when: The seller is motivated by certainty, speed, or tax deferral more than immediate cash.

Why it works: Zero-down entry. You control the asset without needing a bank, a JV partner, or a deposit.

The trade-off: Not every seller will agree. You need to find the right circumstances.

Example: A landlord is retiring with a £1m portfolio. They don’t want to crystallise a massive tax bill in one go. They agree to sell you the portfolio on terms: you pay 20% now, and the balance over five years, with interest. You grow your portfolio without traditional finance.

The professional edge: Vendor finance requires creativity and trust. It’s not advertised on Rightmove. But with the right seller, it’s the ultimate way to scale without limits.

Why Professionals Use All Five

Here’s the mindset shift:

Amateurs ask, “Can I afford it?”

Professionals ask, “What’s the right capital structure for this deal?”

That’s the difference. It’s not about whether you personally have the money. It’s about structuring each opportunity with the optimal mix of capital sources.

One deal might be 70% bank debt, 20% private note, 10% your own cash. Another might be a JV with zero debt. Another might be pure vendor finance.

The point is: you’re never stuck. When you understand the five families, you always have a way forward.

The Trade-Offs: Cost vs Control

Every funding family has its price.

Traditional debt: Cheap, but slow and conservative.

JV equity: Fast, but you give away upside.

Private notes: Flexible, but expensive.

Asset-backed lines: Efficient, but only if you already own assets.

Vendor finance: Creative, but rare.

Professionals don’t avoid these trade-offs. They manage them deliberately.

The Bigger Picture: From Borrower to Allocator

The average landlord is a borrower. They see banks as gatekeepers, and their growth stops when the bank stops.

The professional investor is a capital allocator. They treat money like a toolkit. Each tool has a purpose, and they pick the right one for the job.

That’s why professionals scale portfolios into the hundreds of units while amateurs stall at three.

Final Thought

If you want to play this game seriously, stop asking, “How do I get another mortgage?” and start asking, “Which capital family unlocks this deal?”

Because the future of property isn’t about begging for bank approval. It’s about structuring capital intelligently.

That’s how professionals fund deals without limits.

If you want a real breakdown of how these strategies are used in the field — with case studies, templates, and negotiation tactics — I’ve written it all down in a short, sharp book called Property Unicorn.

And right now, you can get a copy free.

Why You’re Losing £100,000s on Property Deals, And What to Do Instead.

Every week, I meet well-meaning investors — many of them first-time landlords or early-stage buyers — who proudly tell me they’ve secured a couple of shiny new flats off-plan in a so-called “hotspot.” They show me brochures, cite forecasted growth percentages from regional reports, and wait for applause.

But here’s the brutal truth:

Most traditional buy-to-let investors are throwing away hundreds of thousands of pounds over the next decade — all because they’re investing the wrong way.

It’s not because they’re lazy or reckless. It’s because the model they’re following is fundamentally flawed. It’s built on assumptions that no longer hold true in the current market.

The UK property market is full of smart people doing dumb things with good intentions.

Every week, I meet well-meaning investors, many of them first-time landlords or early-stage buyers, who proudly tell me they’ve secured a couple of shiny new flats off-plan in a so-called “hotspot.” They show me brochures, cite forecasted growth percentages from regional reports, and wait for applause.

But here’s the brutal truth:

Most traditional buy-to-let investors are throwing away hundreds of thousands of pounds over the next decade, all because they’re investing the wrong way.

It’s not because they’re lazy or reckless. It’s because the model they’re following is fundamentally flawed. It’s built on assumptions that no longer hold true in the current market.

Let’s unpack this, and more importantly, let me show you a better way.

The Standard Buy-to-Let Blueprint (And Why It’s Broken)

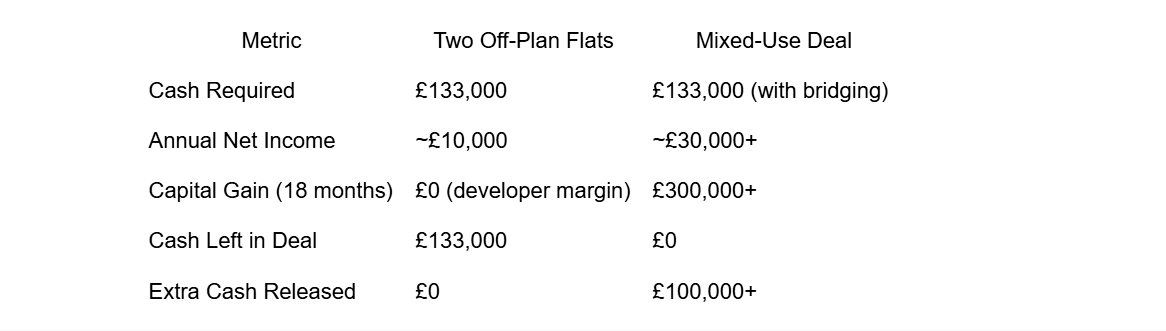

Let’s say you have £100,000 to invest in property, a typical figure for many first-time investors, family landlords, or people cashing in a pension lump sum.

The advice they’re often given is simple:

“Put down 25% deposits on a couple of new-build flats in a regeneration area. Let them out. Hold for capital growth.”

Sounds solid. Let’s run the numbers.

Take this real listing in the North West — a region heavily marketed for “growth potential”:

Price: £200,000 per unit

Deposit (25%): £50,000

Plus SDLT, legal fees, mortgage setup, furnishing, etc.: ~£16,500

Total cash required for two units: ~£133,000

So far, so typical.

Now, what do these flats return?

Gross Rent per unit: ~£10,000/year

Mortgage interest: ~£5,000/year

Net profit per flat (before tax, voids, and maintenance): ~£5,000

Total net return on capital: £10,000/year or ~7.5% gross / ~2.15% net yield on cash invested

And this is best-case scenario before tax and assuming no repairs or voids.

Here’s the kicker: investors are told that a 28.8% growth forecast over the next 5 years will make this model work.

But this thinking is backwards.

Why?

Because they’ve paid full market (or developer-inflated) price. If the value does rise 30% over 5 years, that simply brings them back to true market value, not ahead of it.

They’re not banking profits. They’re just clawing back the premium they overpaid in the first place.

A Better Model: Create Value, Don’t Wait for It

Let’s take the exact same cash, £133,000 and apply a different model.

In 2023, I purchased a tired mixed-use building for £345,000. It wasn’t flashy. It wasn’t off-plan. But it had something far more valuable:

➡️ Undervalued income potential.

We spent around £75,000 on light cosmetic upgrades. Nothing structural. No planning permission. No new build complications. Just:

White-boxing the retail unit to make it lettable

Re-engineering the tenancy structure for efficiency

Modernising the internals with simple layout tweaks

Within 18 months:

The building was independently valued at £750,000+

It now generates £5,000+ per month in rent

We used open-market bridging finance to buy and refurbish

On refinance, the new valuation allowed us to pull out our original £133,000, plus an additional £100,000 in working capital

That’s £233,000 in the bank, a cashflowing asset, and none of our original money left in the deal.

Let’s compare that to the two off-plan flats.

The Hidden Problem With “Safe” Investments

Off-plan and turnkey buy-to-lets are marketed as “hands-off,” “low-risk,” and “guaranteed growth.”

But let’s be honest, when a developer offers a guaranteed rent, it’s not a gift. It’s priced into the sale. And when you buy something brand new, you’re not buying value, you’re buying someone else’s margin.

Here’s the uncomfortable truth:

You are the exit strategy for someone else’s value-add model.

They bought the land cheap, got planning uplift, built at scale, added margin, and now sell to retail investors who believe they’re securing “growth.”

By contrast, the Unicorn Model I use is about finding assets that are:

Undervalued at purchase

Capable of income or layout re-engineering

Able to refinance based on real, forced uplift, not speculation

This allows you to get your capital back fast, and then reuse it, again and again.

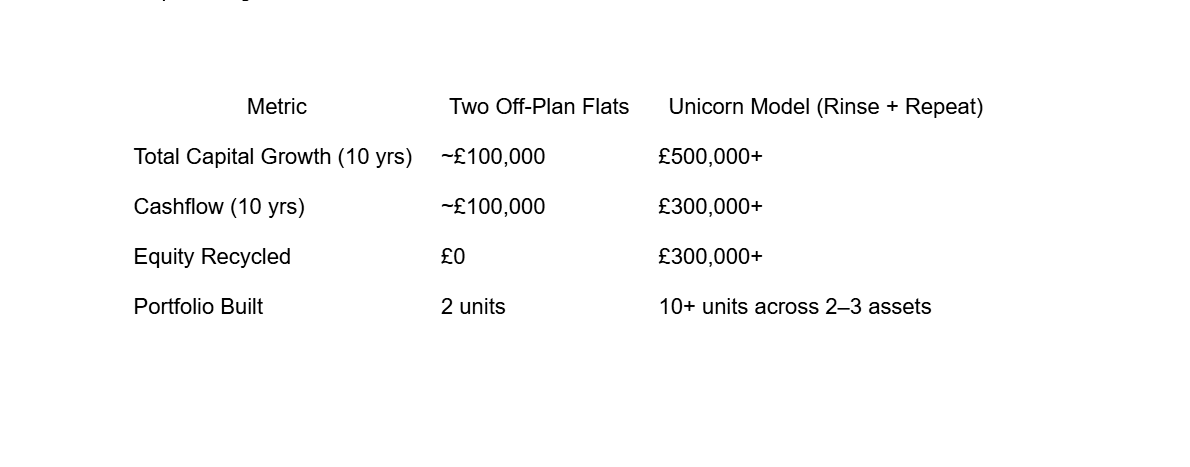

The Real Power of Rinse-and-Repeat

After refinancing that first deal, we used the surplus capital to buy a block of seven flats.

That block now rents for over £100,000 per year. The cash pot that was tied up in two underperforming flats in the mainstream model now controls:

A cashflowing mixed-use asset

A block of 7 residential units

A combined income stream over £130,000/year

Equity growth from two assets

That’s the difference between buying like a landlord and thinking like a developer.

And we did it all with the same original £133,000 that would’ve gone into two off-plan boxes.

Let’s Talk Compounding

The final point most investors miss is this: compounding only works when your capital can move.

When your cash is locked in a deal, even a good one, it’s not compounding. It’s stagnating.

By extracting your capital through refinance, you keep your capital in motion, and that’s when compounding kicks in.

Let’s compare the 10-year outlook of the two models, assuming just 4% annual growth (far below the 28.8% some are sold on):

Final Word: Don’t Buy Property. Engineer It.

Stop buying what’s being sold to you.

Stop waiting for growth to save a poor decision.

Stop assuming that “property always goes up” is a strategy.

What worked for landlords in 2005 does not work in 2025.

The gap between high-street investor and high-performing operator is widening. You either learn how to play like a pro,or you become someone else’s exit.

The good news?

This model isn’t a secret.

It’s not a gimmick.

It’s not reserved for developers in suits with six-figure bank accounts.

It’s systemised, repeatable, and fully explained in my book, Property Unicorn.

📘 Want the full step-by-step playbook?

I’ll send you a free copy of the book. Just hit the link and request it. No charge — just the system we use, backed by real numbers, that works in today’s market.

Stop hoping. Start engineering.

— Rob

5 Creative Finance Hacks You Won’t Hear From the Property Gurus

5 Creative Finance Hacks You Won’t Hear From the Property Gurus

Let’s be honest — most people teaching property today are stuck in the 2010s.

They’re still banging the drum about buy-to-lets, flipping for crumbs, or trying to squeeze ROI out of overpriced terraces with vanilla mortgages. Meanwhile, the reality of 2025 looks very different: tighter credit, higher rates, slower market movement — and a need for smarter, faster, more flexible finance.

That’s where creative finance comes in.

Let’s be honest, most people teaching property today are stuck in the 2010s.

They’re still banging the drum about buy-to-lets, flipping for crumbs, or trying to squeeze ROI out of overpriced terraces with vanilla mortgages. Meanwhile, the reality of 2025 looks very different: tighter credit, higher rates, slower market movement, and a need for smarter, faster, more flexible finance.

That’s where creative finance comes in.

Not as a workaround for people with “no money”, that’s guru bait. No, these strategies are for real investors who want to scale quickly, ethically, and efficiently without being bottlenecked by deposit requirements or debt ceilings.

Here are five proven creative finance tools I teach inside my Property Unicorn program, not theory, but strategies I use in real deals, with real numbers, right now.

1. Lease Option Agreements

Control now, own later, without debt or JV headaches.

The concept is simple, but devastatingly effective: you lease a property today, and secure the right (not the obligation) to buy it at a fixed price in the future. It’s essentially a “delayed completion” deal with upside protection baked in.

✅ Why it works:

You benefit from market appreciation, rental income, and capital uplift without needing a mortgage or deposit up front. No legal title means minimal friction, but full control over cashflow and value.

Who it works for:

Sellers with stalled listings, tired landlords, or developers with surplus stock often prefer this over waiting for a sluggish buyer market.

The deeper strategy:

You can add value during the lease term, change the use, secure planning, or reconfigure layouts, before you ever buy the building. That’s value-creation without capital exposure.

2. Balance Sheet Hacking

Acquire the company, not the property.

This is one of the most underused, and misunderstood, strategies in UK property. Rather than buying the asset, you buy the Ltd company that already owns it. In doing so, you step into their balance sheet, their existing mortgage, and sometimes even their contracts.

✅ Why it works:

You avoid mortgage reapplication, valuation delays, and often save on SDLT (because you're buying shares, not bricks). You inherit existing terms, which can be a game-changer if the original finance was favourable.

The catch:

You must forensically audit the company accounts. This isn’t a trick, it’s a legitimate M&A strategy used by corporate investors for decades. But you need solid legal and financial oversight to do it safely.

The deeper benefit:

This lets you scale faster than your personal debt capacity allows. It’s institutional thinking, applied by nimble operators.

3. 100% Bridging on Open Market Value

Finance the full value, not just the purchase price.

Most investors use bridging for speed, but they forget its greatest strength is in asset-backed lending. If a deal is genuinely undervalued, some lenders will bridge against the full open market value, not just what you're paying.

✅ Why it works:

If you’re buying for £300K and the property’s worth £400K on a valuer’s report, you can borrow the full purchase price, zero money down. This lets you move quickly, secure rare deals, and recycle capital with minimal friction.

Key point:

This only works when the deal is demonstrably below market value, so your ability to source and negotiate well is everything.

Hidden bonus:

Once you control the asset, refinance onto a lower-rate term product, and you’ve created instant equity — and set yourself up for long-term cashflow with no dilution.

4. Vendor Deposit Deferment

Pay the deposit from future profits.

Sometimes, the simplest thing is to just ask the vendor to wait.

If the deal is right — and you’ve shown credibility — you can structure an agreement where the seller defers all or part of your deposit until income starts rolling in. You complete the transaction but pay the balance after a set term.

✅ Why it works:

Most people assume deposits must come from savings or investors. But if you offer the seller certainty and speed, they’ll often trade for delayed payment — especially if they’re not under time pressure.

When it works best:

On off-market deals, tired portfolios, or commercial-to-resi conversions where the vendor sees the long-game.

The real play:

Use the rent to pay the deposit, and you’ve effectively created a zero-cash-flow-to-control transition. That’s how smart investors scale without waiting on capital.

5. Exchange Subject to Planning

Lock in today’s price. Add value before you even own it.

With this technique, you exchange contracts today, but only complete the purchase once you’ve secured planning permission, or whatever other milestone you agree on.

✅ Why it works:

You reduce risk by not committing to the full purchase unless value is guaranteed to increase. It’s perfect for deals where planning uplift, lease restructuring, or permitted development plays are on the table.

Use it strategically:

Negotiate a long completion window. Push value through during the delay. Then complete with equity already baked in, often with higher leverage options thanks to the improved GDV.

The nuance:

This method puts you in value-creator mode, not just buyer mode. And that’s where the real profits are made.

Final Thought: Don’t Follow the Crowd, Design the Game

Every single one of these strategies has helped me, and my students, unlock deals most investors walk past.

The difference?

We’re not playing the game the banks, the gurus, or the system want you to play. We’re designing our own rules, using leverage intelligently, controlling risk, and creating value before we commit capital.

This isn’t about “getting rich quick.” It’s about getting free from the traditional model, one deal at a time.

Let me know in the comments which of these you’ve used or want to learn more about.

And if you're serious about deploying Unicorn Momentum into your next deal, I’ve got the templates, scripts, and real-life examples waiting, just ask.

Until then:

Think less about how many properties you own.

And more about how creatively you control them.

— Rob

Bank Rate Stalled at 4.25%? How 6% Mortgages Let You Unlock £100k+ in Equity with Property Unicorns.

Yet now, Governor Andrew Bailey cautions that while the trajectory remains downward, “how far and how quickly” those cuts arrive is “shrouded in uncertainty.” His message is clear: inflation isn’t collapsing as hoped (it sat near 3.5% in April), wage pressures are still high, and global trade frictions linger.

Imagine it’s May 2025, and everyone thought the Bank of England would slice interest rates at least three more times this year, potentially as soon as its June meeting.

Market predictions of a sub-4 % base rate (with some even calling for 3.5% by the end of the year) seemed inevitable.

Yet now, Governor Andrew Bailey cautions that while the trajectory remains downward, “how far and how quickly” those cuts arrive is “shrouded in uncertainty.” His message is clear: inflation isn’t collapsing as hoped (it sat near 3.5% in April), wage pressures are still high, and global trade frictions linger.

In other words, a June cut may be pushed into August or later, and perhaps only a single 25-basis-point trim in 2025 rather than the two to three everyone expected.

That “pause” in rate cuts might feel like unwelcome news for would-be homebuyers hoping for cheaper mortgages. But if you’re the type who hunts mixed-use buildings — what I call “Property Unicorns” — this slower-than-expected path lights up an opportunity.

Why?

Because when borrowing costs stay elevated for a little longer, buyers who crave 3% mortgages hold off, sellers face a reality check on pricing, and smaller, hands-on investors like us can swoop in on underpriced deals without a stampede of big-money competition.

Think of a Property Unicorn as a modest block — four flats upstairs and a little shop or office downstairs — where you invest a relatively small sum (say £50,000) in smart refurbishments and lease negotiations. Within six months, those improvements push rental income up by 15–20%. A surveyor then looks at the higher rent roll and says, “This building is worth more,” effectively bumping the valuation by significantly more than the amount you spent.

You didn’t need to wait for mortgage rates to plunge; you engineered that value yourself, all while collecting £3,000 (or more) per month in net cashflow.

To see why this works so well in a “slow-cut” scenario, let’s rewind to earlier in 2025.

After trimming Bank Rate from 4.50 to 4.25% in May, most analysts thought a 4.00% rate was coming in June. Swap curves — those interest rates lenders use to price fixed-rate mortgages — dipped in late April and early May, teasing a broad easing.

But the April inflation print came in at 3.5% — higher than the BoE’s comfort zone — and wage growth in crucial sectors (healthcare, construction, logistics) remained sticky at nearly 5%. Combine that with fresh trade-policy uncertainty from U.S. tariffs and global supply-chain jitters, and Bailey felt compelled to dial back expectations. He’s publicly said the MPC wants to be “gradual and careful,” ensuring any future cuts don’t undo the fight against lingering inflation.

In practical terms, that means mortgage rates won’t tumble in June as once hoped. Instead, two-year fixed deals hover near 5.05%, five-year fixes around 5.15%. Back in 2021, those figures were often 1.50–2.00%.

So for a would-be buyer, £300,000 over 25 years at 5.15% equals roughly £1,800 per month. If the rate fell to 5.00%, payments only drop to around £1,750 — a mere £50 saving. Hardly a dramatic improvement, and not enough to spark a housing frenzy.

Bolstered by that realism, sellers who had priced homes and small shops assuming imminent 4.00% rates now reset expectations. If they want to transact in mid-2025, they must accept that high financing costs will remain part of the landscape. That, in turn, prompts some sellers to negotiate rather than hold out for a distant, hypothetical plunge to 3.50%.

In this environment, unicorn deals shine because you don’t hinge on broad market swings — you build value with your own hands.

Imagine spotting a block in Sheffield: four flats each renting for £7,500 per year, plus a ground-floor shop at £10,000, total income £40,000. The asking price is £420,000, implying a 9.5% yield.

At first glance, a 9.5% in May 2025 means serious rental upside, especially when comparable flats in the same area already achieve £9,000 to £9,500 per year. With a modest budget — say, £50,000 — you can modernise each flat (new kitchen, bathroom refresh, fresh paint) and spruce up the shop (new signage, minor façade work). That refurbishment takes about eight weeks.

Once complete, you re-let all four flats at £9,500 each — £38,000 in residential rent — then sign the shop to a new café operator at £13,000 per year. Your post-refurb rent roll jumps from £40,000 to £51,000 — an eye-popping 27.5% increase.

A surveyor, seeing that £51,000 in annual income, might apply a 7% capitalisation rate (a typical yield for a well-let, modernised mixed‐use block in a secondary city). At 7%, that rent roll suggests a value of about £730,000.

In reality, if you sell quickly, you might net offers around £700,000, leaving a small discount for a quick sale. Even so, you’ve taken £420,000 + £50,000 (= £480,000) in total commitment and turned it into an asset valued at over £700,000 in six months — an instant £220,000+ equity boost.

Meanwhile, finance costs remain high — if you borrowed 60% of £420,000 (≈£252,000) at a 6% interest-only rate, your annual interest is £15,120 (≈£1,260 per month). After letting expenses, insurance and maintenance (say about £10,000 per year), you clear roughly £25,880 per year — or about £2,156 a month.

When the BoE eventually cuts in August (or September if the data continues to frustrate), commercial mortgage rates might fall to ub 6%. That slight drop helps with refinance costs. You’d approach a lender in late 2025 with your newly proven rent roll: “Look, this building nets £25,000 per year after operating costs and interest at 6%; at 5.5% on a new valuation of £700,000, I can refinance 60% and extract roughly £420,000 of equity.”

You repay the old loan (£252,000), pocket about £168,000 in extracted equity, and roll that into your next Unicorn.

This means you now only have £50,000 of your original funds left in the deal, which is still producing a net income of £17,9000 (after £10k costs) per year — over 35% net return on capital employed.

By contrast, a traditional buy-to-let investor — putting down a 25% deposit on one £225,000 flat at 5% and getting 4.5% in rent — comes out roughly cashflow neutral. They wait for rates to fall lower, cross their fingers for capital growth, and hope that rental demand remains strong. In a “slow-cut” world, that investor is at the mercy of central banks. Your Unicorn strategy, however, locks in equity from strong rental improvements and your reserve of patience while markets wait for the next cut.

Another reason that slow cuts benefit Unicorn investors is psychological: when cuts are fast and steep, buyers rush in, driving prices above their fundamental value. We observed that in 2021–2022, two-year fixed rates reached around 1.5–2%. Everyone bought, believing rates would stay low indefinitely, and prices soared 15–20% in many places. However, rates reversed quickly, prices stalled, and a correction ensued. With slow cuts, prices move more gently , perhaps just 2–3% later in 2025 and another 3–4% in 2026 , giving you breathing room. Sellers adjust to “5% mortgages are here,” and you can plan, negotiate, renovate, and refinance without the stress of a rapidly shifting market.

That “slow-cut” cushion also keeps vacancy rates low for rentals. Many folks who wanted to buy in May 2025 can’t afford a 5.15% mortgage, so they stay renting. Vacancy rates in strong university towns and commuter hubs remain near 2–3%. In turn, that tight rental market supports your ability to increase flat rents by 20% post-refurb — never a given, but far likelier when demand outstrips supply. On the commercial side, small shops and cafés that might struggle in a booming city centre find a captive audience in a residential block. When you present a freshly updated café or convenience store with solid tenant reference, landlords and lenders view that as a stable income stream. That further bolsters your refinancing pitch.

In a nutshell, the slower-than-expected rate cuts set up a rare window of opportunity. Sellers, who once believed they could fetch top prices if mortgages dipped to 4%, now face the reality of 6% rates persisting. They adjust pricing accordingly, giving us hands-on investors better deals. Big funds, which chase very cheap debt to make slim yields work, hold back, leaving mixed-use blocks to local players.

Meanwhile, rental markets remain firm, commercial mortgage rates are expected to hold at around 6% until at least August, and surveyors continue to value strong rent rolls at reasonable yields (7–8% for updated mixed-use properties). All of this converges to create an ideal environment for Property Unicorns: you can buy at high yields (9–10%), invest £40,000–£50,000 to drive yields down to 7%, and capture that spread in equity.

It’s important to emphasise: you’re not “betting” on rates falling dramatically. Instead, you’re banking on your expertise — finding under-priced blocks, negotiating favourable purchase prices, managing innovative renovations, and securing long-term leases. Even if the BoE delays further cuts until October or November, you still capture most of your uplift through operational improvements. When banks finally do offer a slightly improved refinance rate — say, 5.5 %— you pocket that incremental advantage on top of your expertly generated equity.

People often ask, “Isn’t it too risky to buy a small mixed-use building when rates are still high?” The answer is that risk is relative. A standard buy-to-let flat at 4% yield — when you’re borrowing at 5%— leaves you vulnerable. You might be cash flow neutral or slightly negative until rates fall by two whole points. With a Unicorn, you start at a 9–10% yield. You know exactly how much rent you’ll achieve after renovation. You forecast refinancing at 5.5% per cent. You build in a safety buffer , covering one or two months of void via reserves. And fundamentally, you’re not speculating on Brexit shocks or pandemic rolls, but on concrete on-the-ground improvements: new kitchens, fresh bathrooms, better tenant quality. That level of control makes your risk profile quite manageable.

Looking ahead to late 2025 and early 2026, once inflation drifts further toward 2.5 per cent and wage growth eases, the BoE is likely to trim the Bank Rate to 4.00 per cent in August and 3.75 per cent by early 2026. That may nudge five-year resi fixes down to near 4.75–4.90 per cent — certainly better than today’s 5.15 per cent. Commercial mortgages should follow suit.

By then, you will already have executed your Unicorn strategy: bought, renovated, re-let, and either sold or refinanced. So you capture both your hands-on value creation and any remaining yield compression. Meanwhile, house prices might creep up only 2–3 percent in late 2025 and 3–4 per cent in 2026 — hardly a blistering boom, but enough that your long-term hold has further upside beyond your immediate equity gain.

In short, May 2025’s “shrouded path” of rate cuts is not a deterrent — it’s a clarion call. When everyone else waits for a perfectly timed decline, you, the Property Unicorn hunter, move on the deals that exist now. You negotiate while big funds twiddle their thumbs. You create equity when sellers reluctantly accept that 5 per cent mortgages are here to stay. And you refinance at a slightly better rate when the BoE eventually bends — pocketing a tidy profit and steady cashflow along the way.

If this resonates and you want the full, step-by-step playbook — detailed case studies, budgeting templates, negotiating scripts, refurbishment checklists, refinance strategies — grab a copy of Property Unicorns.

Inside, you’ll learn exactly how to turn uncertainty into opportunity, build your equity ladder one block at a time, and thrive, even when the Bank of England’s path remains uncertain. When a rate cut finally arrives, you won’t be scrambling for a deal — you’ll already be on to the next Unicorn.

Just click here now to order your free copy, you just need to cover the £4.97 P&P!

The Broken uk planning system

It all begins wiTake a look at the biggest UK homebuilders — Barratt, Persimmon, Taylor Wimpey, Bellway. These aren’t just property companies; they’re controlled by major institutional investors like BlackRock. Planning laws aren’t about ensuring fair competition; they’re about maintaining the monopoly of big players.

When the government claims to be supporting property development, what they’re really doing is:

Fast-tracking large-scale projects that benefit institutional investors.

Leaving small and mid-sized developers trapped in bureaucracy.

Creating artificial supply shortages to inflate property values.

So, where does that leave us? If you’re a property entrepreneur trying to build a portfolio, create housing solutions, and contribute to the market, you have two choices:

Accept the system is broken and give up.

Adapt, innovate, and disrupt using the Unicorn Model.th an idea.

image from building.co.uk

For years, the UK government has promised to fix the planning system to accelerate economic growth, support development, and address the housing crisis. Yet, here we are — dealing with a fundamentally broken system that stifles innovation, pushes small developers to the side-lines, and hands power to large corporations.

I’m not just another property commentator. I live and breathe this business. I’ve built a successful career by disrupting the status quo and finding solutions where others see roadblocks. Today, I want to talk about how the UK planning system is failing us, who benefits from its dysfunction, and — most importantly — how small developers can still win using my Unicorn Model.

The UK Planning System: A System Designed to Fail.

The UK planning system isn’t just slow — it’s designed in a way that actively prevents small developers from succeeding. I have a project that should have made £200,000 in profit, yet it’s been stuck in planning for nine months. Why? Because of a sudden “planning lockdown” imposed due to phosphate pollution in a river 30 miles away. That’s right — red tape from an unrelated environmental issue has frozen a legitimate, well-planned investment.